House of Travel Insurance

Compare House of Travel Insurance

To compare House of Travel insurance policies with those from other providers on Canstar’s database, follow the link below.

Compare Travel Insurance

What types of travel insurance does house of travel offer.

House of Travel has partnered with Allianz to offer comprehensive insurance cover for its travel clients.

House of Travel has eight travel insurance plans on offer:

- Plan A: Essentials Plus

- Plan B: Premier

- Plan C: Non-residents Incoming to New Zealand

- Plan D: Permanent One-way From New Zealand

- Plan E: Multi-trip

- Plan F: Domestic Cancellation

- Plan G: Domestic Essentials

- Plan H: Residents Returning to New Zealand

What’s covered by House of Travel’s Plan A: Essentials Plus policy?

Plan A is available as a single or family package. Both options come with unlimited overseas emergency medical assistance and hospital expenses.

- $400 per person for overseas dental expenses

- $1500 for continuing medical expenses on return to New Zealand (per person)

- Accidental death cover of $50,000 for singles/$100,000 for families

- Permanent disability cover of $50,000 for singles/$100,000 for families

- Cancellation cover of $10,000 for singles/$20,000 for families

- $4500 for rental vehicle insurance excess

- Up to $2.5 million for personal liability

- Additional expenses up to $50,000 for singles/$100,00 for families

- Alternative transport expenses of $5000 for singles/$10,000 for families

What’s covered by House of Travel’s Plan B: Premier policy?

Plan B is also available as a single or family package. It covers everything that Plan A covers, often with higher compensation, plus extra areas including: dental expenses on return to New Zealand and loss of income.

- Resumption of journey cover of $10,000 for singles/$20,000 for families

- Cancellation cover of $100,000 for singles/$200,000 for families

- Travel delay expenses of $2000 for singles/$4000 for families

- Accidental death cover of $75,000 for singles/$150,000 for families

What’s covered by House of Travel’s Plan C: Incoming to New Zealand Non-residents policy?

Plan C is available for non-residents travelling to New Zealand. Policy holders will receive unlimited overseas emergency medical and hospital expenses, plus cover for additional situations. The policy can be taken out for singles or families.

What’s covered by House of Travel’s Plan D: Permanent One-way From New Zealand policy?

Plan D is available for those moving to New Zealand permanently. This policy can be taken out for singles or families. Singles will be eligible for up to $250,000 for overseas emergency medical and hospital expenses. Families will be eligible for up to $500,000 for the same cover.

What’s covered by House of Travel’s Plan E: Multi-trip policy?

Cover is available under Plan E Multi-trip if all of the following apply:

- You are a resident or temporary resident of New Zealand; and

- You have purchased your policy before commencing your journey; and

- Your journey commences and ends in New Zealand

Policy holders are entitled to unlimited overseas emergency medical and hospital expenses. Other cover includes death, disability, cancellation and personal liability.

What’s covered by House of Travel’s Plan F: Domestic Cancellation policy?

Plan F provides cover for domestic travel cancellation only. Singles are eligible for cover up to $10,000 and families are eligible for cover up to $20,000.

What’s covered by House of Travel’s Plan G: Domestic Essentials policy?

Plan G provides cover for those travelling domestically. Plan G’s policy covers cancellation, personal liability, rental vehicle insurance excess and more.

What’s covered by House of Travel’s Plan H: Residents Returning to New Zealand policy?

Plan H provides cover for New Zealand residents who are overseas and ends when they arrive at any immigration counter in New Zealand.

Plan H provides comprehensive cover for residents and includes unlimited cover for overseas emergency medical and hospital expenses, personal liability, cancellations and additional expenses.

Optional cover available for most plans includes:

- Increased item limits

- Increased rental vehicle insurance excess cover

- Special activity packs

About House of Travel

Established in 1987, House of Travel has grown to be the largest privately owned travel company in New Zealand and the third largest travel organisation in the Asia Pacific region.

Currently House of Travel employs more than 2000 staff across 75 travel stores across the country.

Written by: Caitlin Bingham | Last updated: November 23, 2023

Other Travel Insurance from

House of Travel

Southern Cross

Compare Outstanding Value Travel Insurance

Compare Travel Insurance By Destination

Outstanding Value Travel Insurance Awards

Canstar's Best Value Travel Insurance NZ

Wise: the Best Travel Money Card in New Zealand

Do I Need Travel Insurance to Visit Australia?

Quick Links

The best travel insurance policies and providers

It's easy to dismiss the value of travel insurance until you need it.

Many travelers have strong opinions about whether you should buy travel insurance . However, the purpose of this post isn't to determine whether it's worth investing in. Instead, it compares some of the top travel insurance providers and policies so you can determine which travel insurance option is best for you.

Of course, as the coronavirus remains an ongoing concern, it's important to understand whether travel insurance covers pandemics. Some policies will cover you if you're diagnosed with COVID-19 and have proof of illness from a doctor. Others will take coverage a step further, covering additional types of pandemic-related expenses and cancellations.

Know, though, that every policy will have exclusions and restrictions that may limit coverage. For example, fear of travel is generally not a covered reason for invoking trip cancellation or interruption coverage, while specific stipulations may apply to elevated travel warnings from the Centers for Disease Control and Prevention.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that may fit your travel needs.

So, before buying a specific policy, you must understand the full terms and any special notices the insurer has about COVID-19. You may even want to buy the optional cancel for any reason add-on that's available for some comprehensive policies. While you'll pay more for that protection, it allows you to cancel your trip for any reason and still get some of your costs back. Note that this benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

In this guide, we'll review several policies from top travel insurance providers so you have a better understanding of your options before picking the policy and provider that best address your wants and needs.

The best travel insurance providers

To put together this list of the best travel insurance providers, a number of details were considered: favorable ratings from TPG Lounge members, the availability of details about policies and the claims process online, positive online ratings and the ability to purchase policies in most U.S. states. You can also search for options from these (and other) providers through an insurance comparison site like InsureMyTrip .

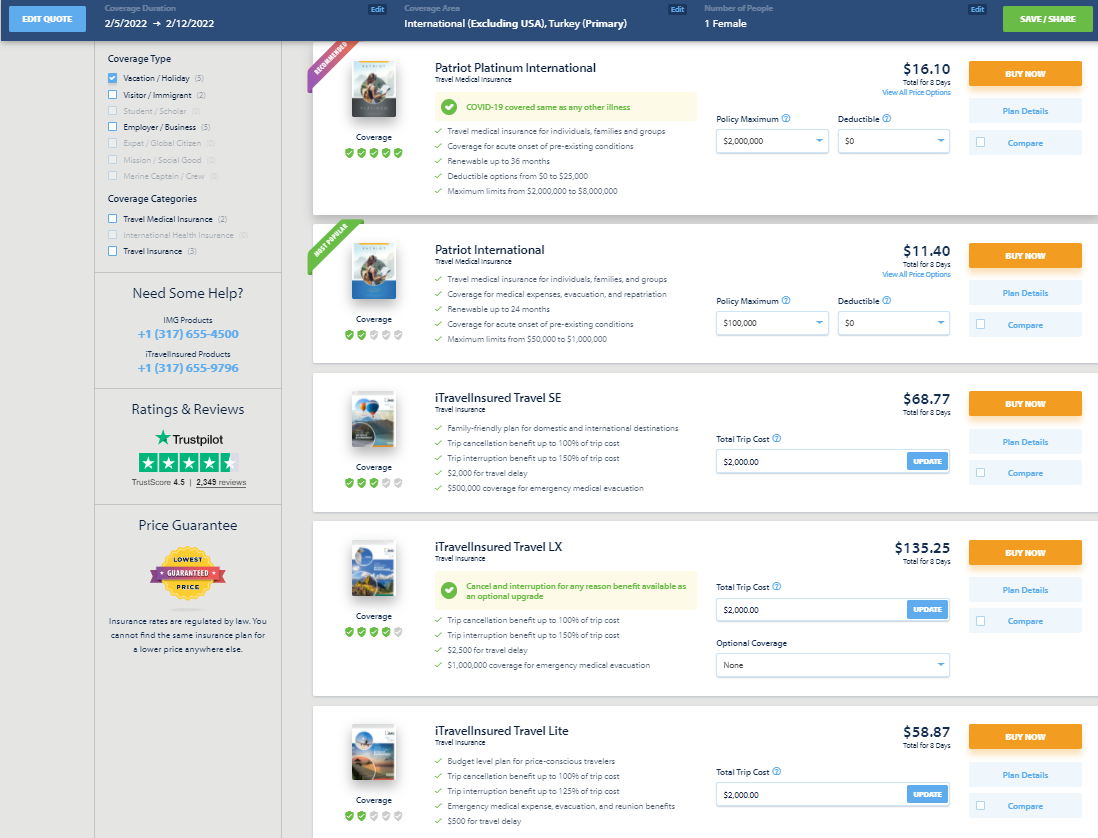

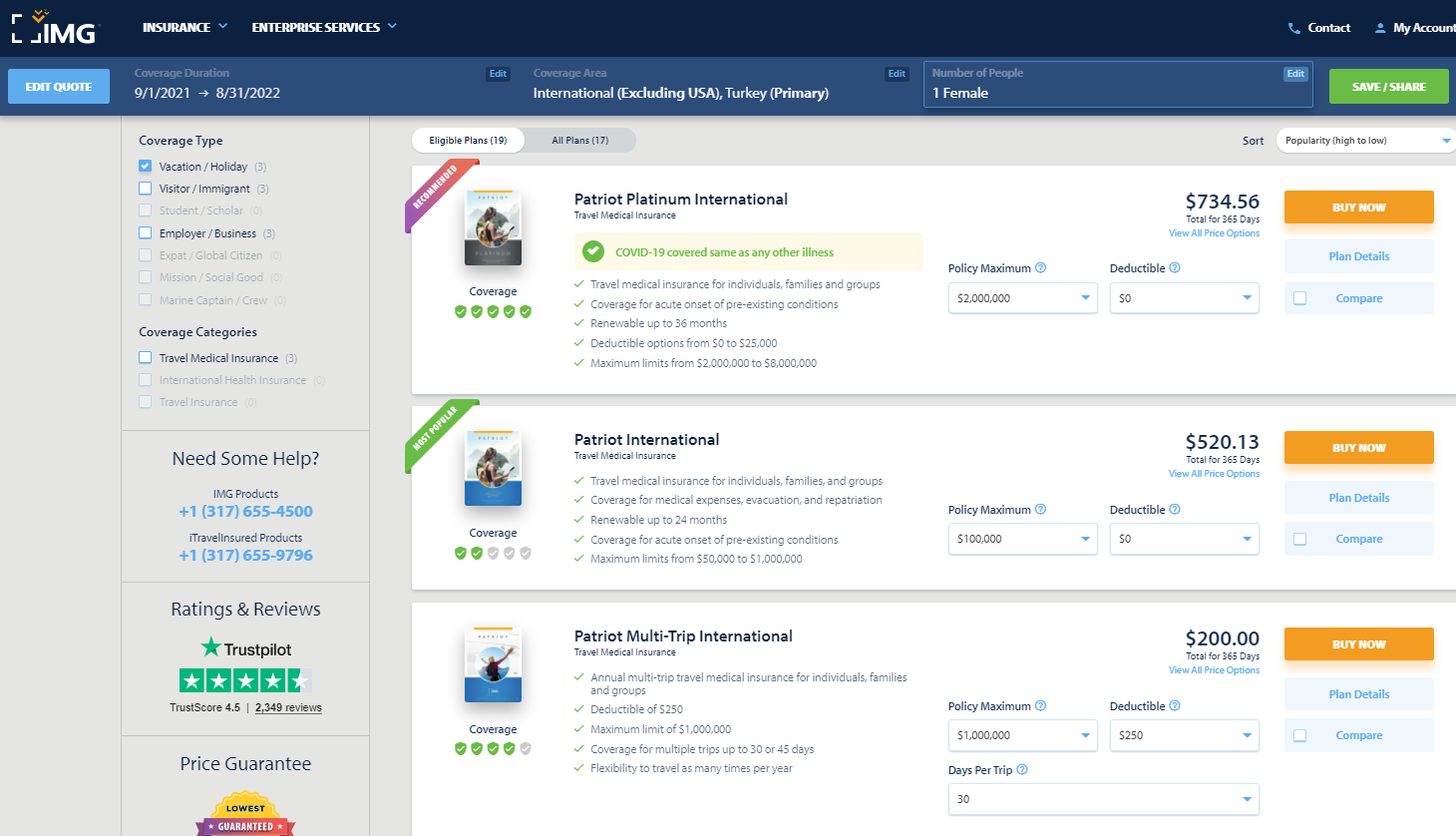

When comparing insurance providers, I priced out a single-trip policy for each provider for a $2,000, one-week vacation to Istanbul . I used my actual age and state of residence when obtaining quotes. As a result, you may see a different price — or even additional policies due to regulations for travel insurance varying from state to state — when getting a quote.

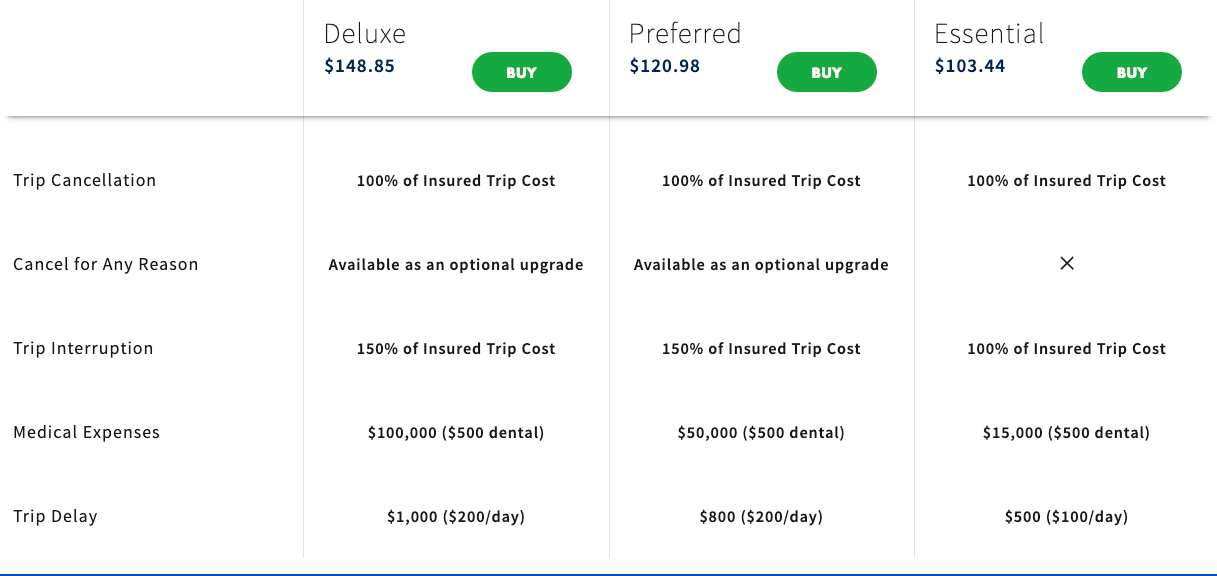

AIG Travel Guard

AIG Travel Guard receives many positive reviews from readers in the TPG Lounge who have filed claims with the company. AIG offers three plans online, which you can compare side by side, and the ability to examine sample policies. Here are three plans for my sample trip to Turkey.

AIG Travel Guard also offers an annual travel plan. This plan is priced at $259 per year for one Florida resident.

Additionally, AIG Travel Guard offers several other policies, including a single-trip policy without trip cancellation protection . See AIG Travel Guard's COVID-19 notification and COVID-19 advisory for current details regarding COVID-19 coverage.

Preexisting conditions

Typically, AIG Travel Guard wouldn't cover you for any loss or expense due to a preexisting medical condition that existed within 180 days of the coverage effective date. However, AIG Travel Guard may waive the preexisting medical condition exclusion on some plans if you meet the following conditions:

- You purchase the plan within 15 days of your initial trip payment.

- The amount of coverage you purchase equals all trip costs at the time of purchase. You must update your coverage to insure the costs of any subsequent arrangements that you add to your trip within 15 days of paying the travel supplier for these additional arrangements.

- You must be medically able to travel when you purchase your plan.

Standout features

- The Deluxe and Preferred plans allow you to purchase an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% or 75% of your covered trip cost.

- You can include one child (age 17 and younger) with each paying adult for no additional cost on most single-trip plans.

- Other optional upgrades, including an adventure sports bundle, a baggage bundle, an inconvenience bundle, a pet bundle, a security bundle and a wedding bundle, are available on some policies. So, an AIG Travel Guard plan may be a good choice if you know you want extra coverage in specific areas.

Purchase your policy here: AIG Travel Guard .

Allianz Travel Insurance

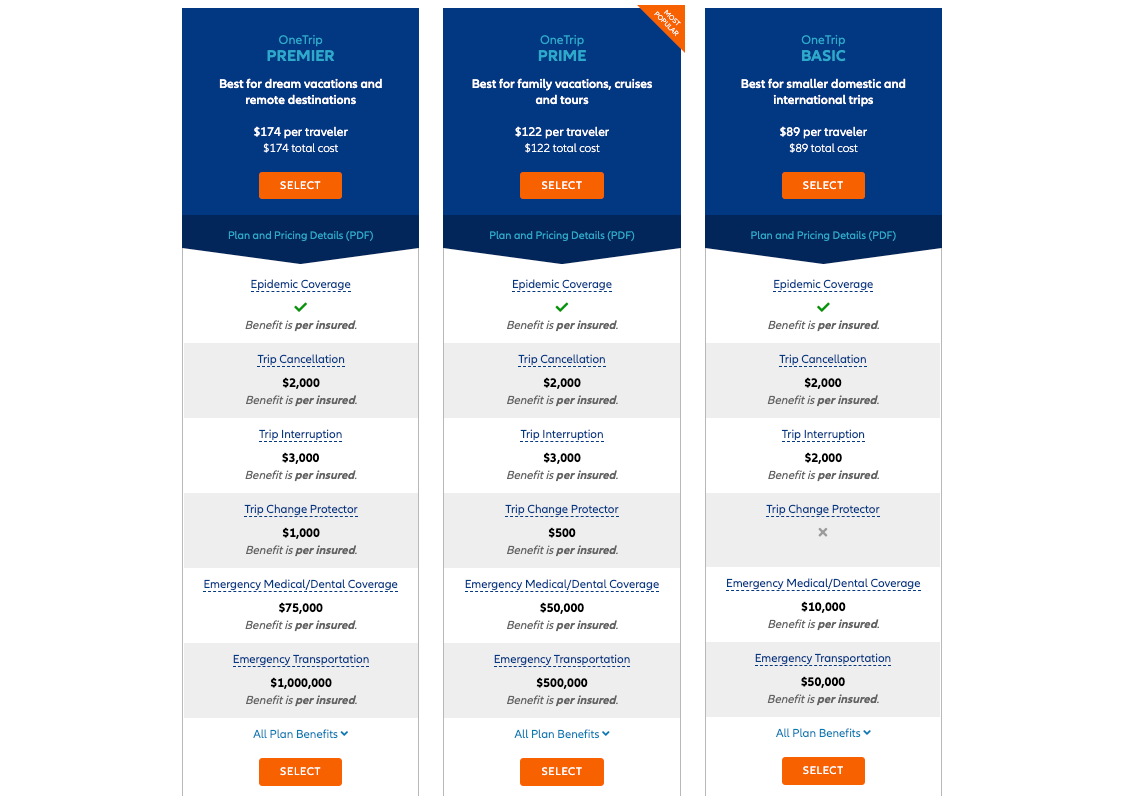

Allianz is one of the most highly regarded providers in the TPG Lounge, and many readers found the claim process reasonable. Allianz offers many plans, including the following single-trip plans for my sample trip to Turkey.

If you travel frequently, it may make sense to purchase an annual multi-trip policy. For this plan, all of the maximum coverage amounts in the table below are per trip (except for the trip cancellation and trip interruption amounts, which are an aggregate limit per policy). Trips typically must last no more than 45 days, although some plans may cover trips of up to 90 days.

See Allianz's coverage alert for current information on COVID-19 coverage.

Most Allianz travel insurance plans may cover preexisting medical conditions if you meet particular requirements. For the OneTrip Premier, Prime and Basic plans, the requirements are as follows:

- You purchased the policy within 14 days of the date of the first trip payment or deposit.

- You were a U.S. resident when you purchased the policy.

- You were medically able to travel when you purchased the policy.

- On the policy purchase date, you insured the total, nonrefundable cost of your trip (including arrangements that will become nonrefundable or subject to cancellation penalties before your departure date). If you incur additional nonrefundable trip expenses after purchasing this policy, you must insure them within 14 days of their purchase.

- Allianz offers reasonably priced annual policies for independent travelers and families who take multiple trips lasting up to 45 days (or 90 days for select plans) per year.

- Some Allianz plans provide the option of receiving a flat reimbursement amount without receipts for trip delay and baggage delay claims. Of course, you can also submit receipts to get up to the maximum refund.

- For emergency transportation coverage, you or someone on your behalf must contact Allianz, and Allianz must then make all transportation arrangements in advance. However, most Allianz policies provide an option if you cannot contact the company: Allianz will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Allianz Travel Insurance .

American Express Travel Insurance

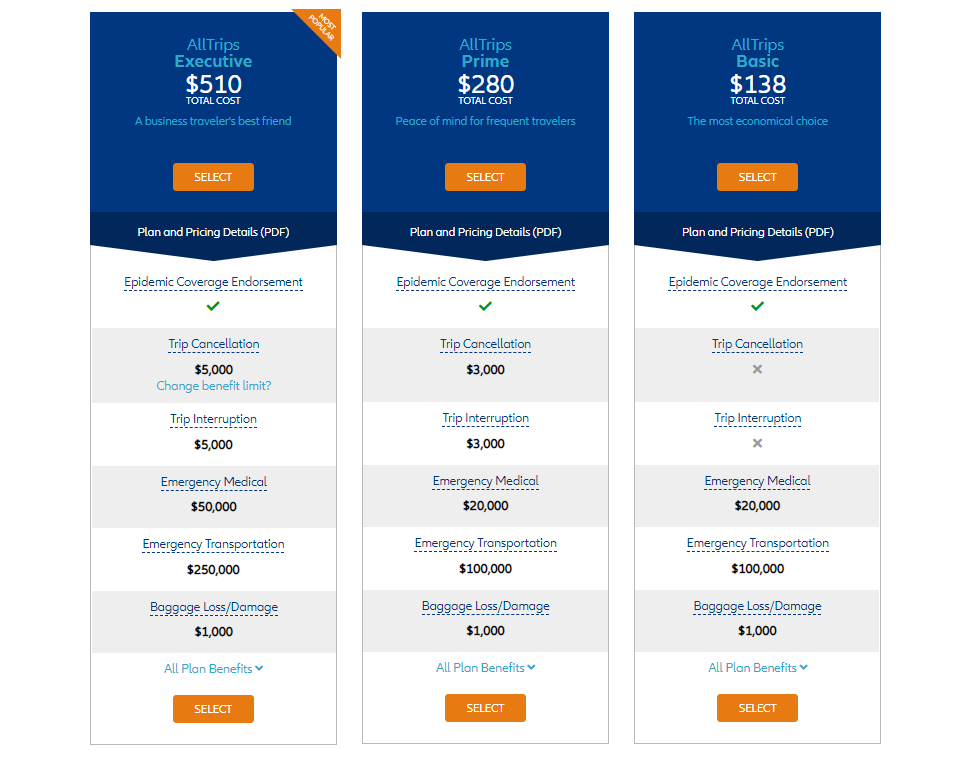

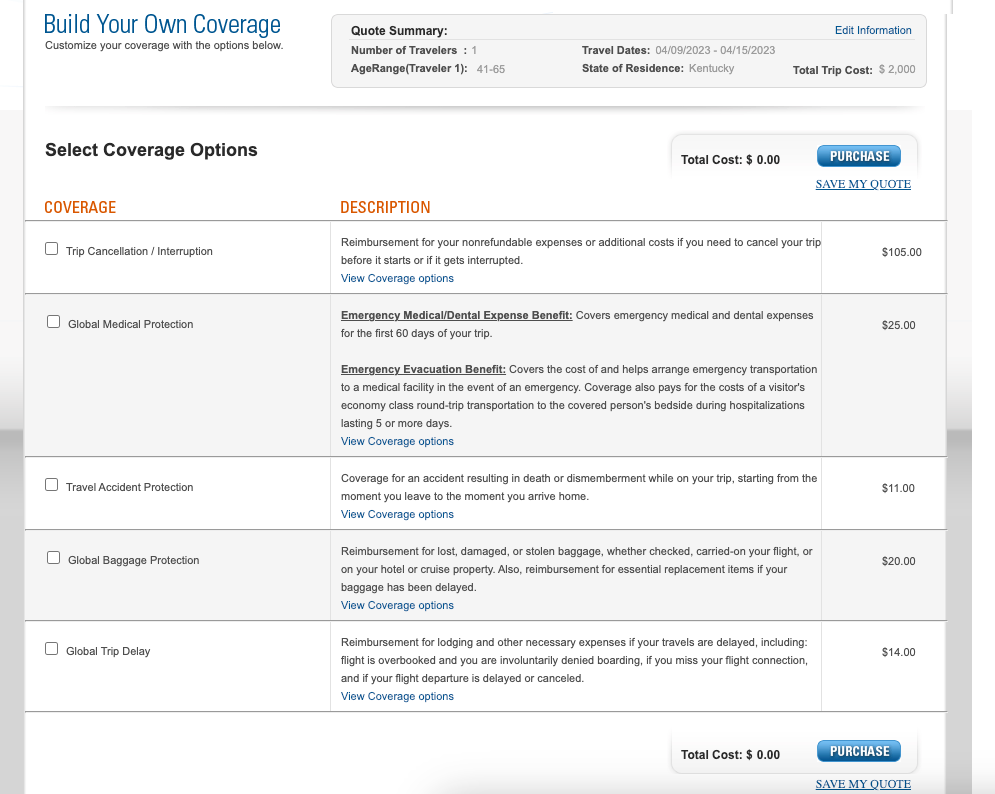

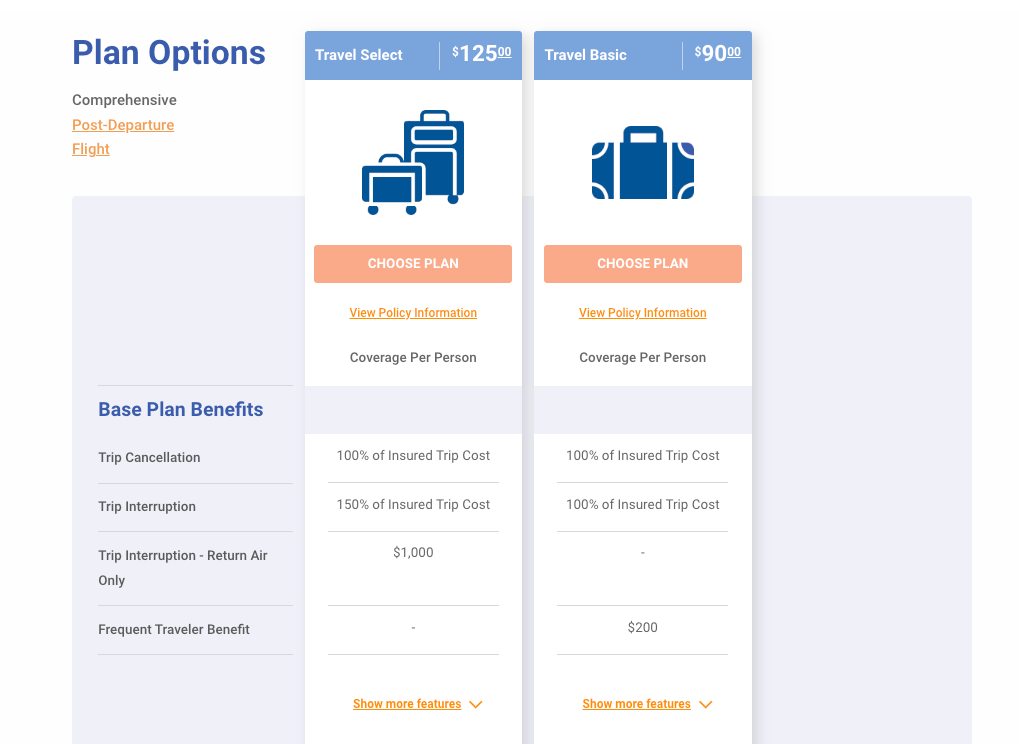

American Express Travel Insurance offers four different package plans and a build-your-own coverage option. You don't have to be an American Express cardholder to purchase this insurance. Here are the four package options for my sample weeklong trip to Turkey. Unlike some other providers, Amex won't ask for your travel destination on the initial quote (but will when you purchase the plan).

Amex's build-your-own coverage plan is unique because you can purchase just the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

The prices for the packages and the build-your-own plan don't increase for longer trips — as long as the trip cost remains constant. However, the emergency medical and dental benefit is only available for your first 60 days of travel.

Typically, Amex won't cover any loss you incur because of a preexisting medical condition that existed within 90 days of the coverage effective date. However, Amex may waive its preexisting-condition exclusion if you meet both of the following requirements:

- You must be medically able to travel at the time you pay the policy premium.

- You pay the policy premium within 14 days of making the first covered trip deposit.

- Amex's build-your-own coverage option allows you to only purchase — and pay for — the coverage you need.

- Coverage on long trips doesn't cost more than coverage for short trips, making this policy ideal for extended getaways. However, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other types of points and miles aren't covered.

Purchase your policy here: American Express Travel Insurance .

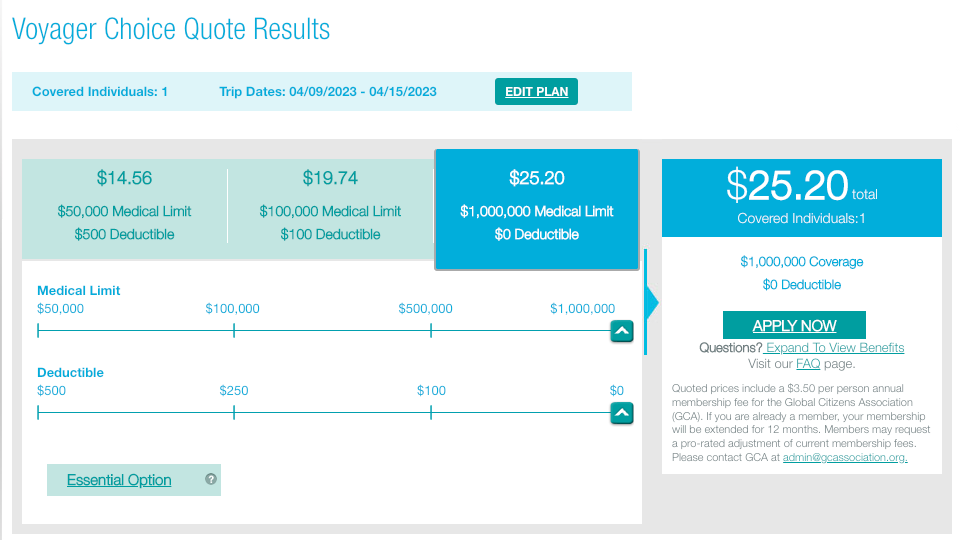

GeoBlue is different from most other providers described in this piece because it only provides medical coverage while you're traveling internationally and does not offer benefits to protect the cost of your trip. There are many different policies. Some require you to have primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), but all of them only offer coverage while traveling outside the U.S.

Two single-trip plans are available if you're traveling for six months or less. The Voyager Choice policy provides coverage (including medical services and medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger and already have a U.S. health insurance policy.

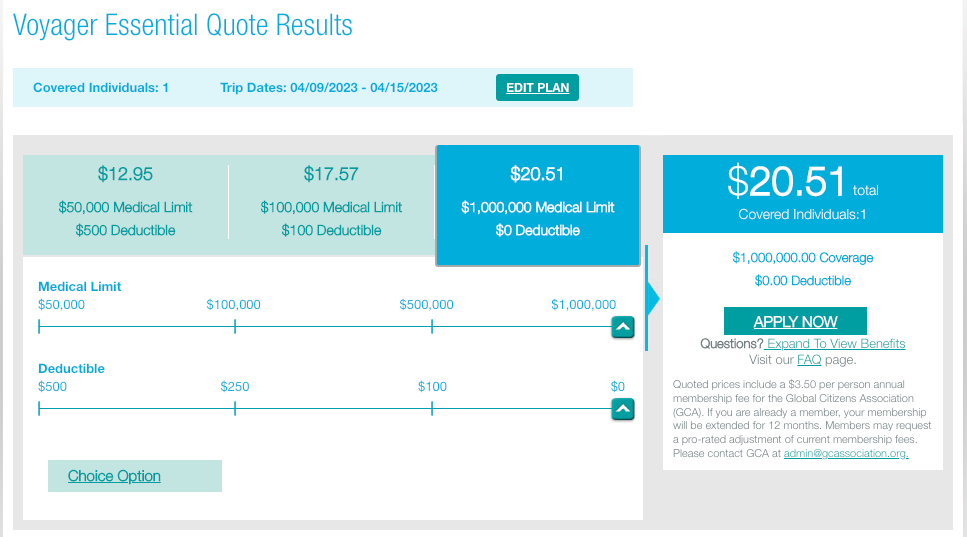

The Voyager Essential policy provides coverage (including medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger, regardless of whether they have primary health insurance.

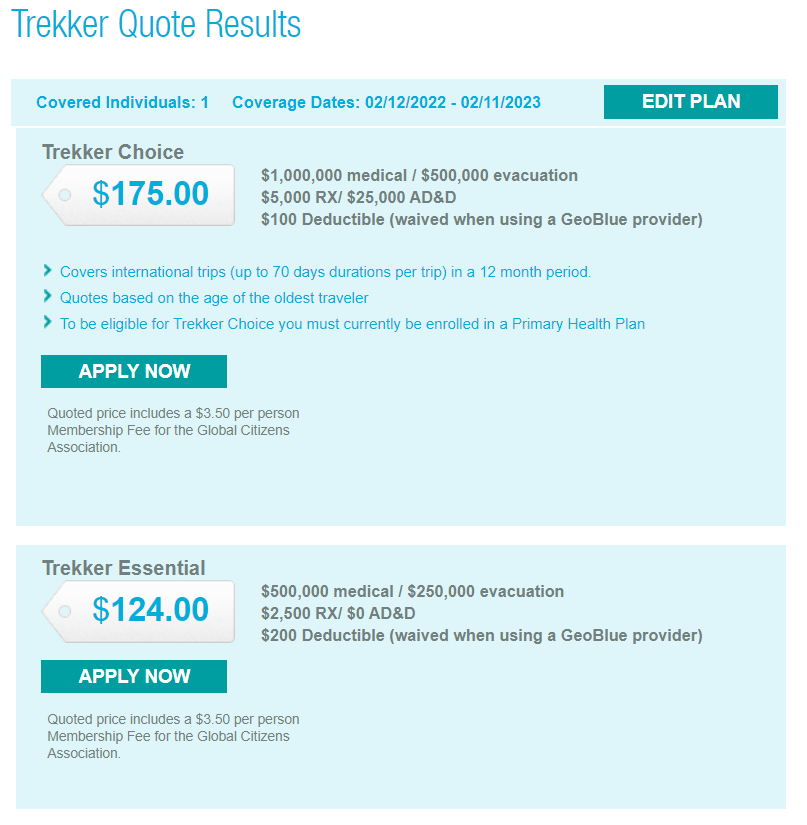

In addition to these options, two multi-trip plans cover trips of up to 70 days each for one year. Both policies provide coverage (including medical services and medical evacuation for preexisting conditions) to travelers with primary health insurance.

Be sure to check out GeoBlue's COVID-19 notices before buying a plan.

Most GeoBlue policies explicitly cover sudden recurrences of preexisting conditions for medical services and medical evacuation.

- GeoBlue can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- GeoBlue provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

Purchase your policy here: GeoBlue .

IMG offers various travel medical insurance policies for travelers, as well as comprehensive travel insurance policies. For a single trip of 90 days or less, there are five policy types available for vacation or holiday travelers. Although you must enter your gender, males and females received the same quote for my one-week search.

You can purchase an annual multi-trip travel medical insurance plan. Some only cover trips lasting up to 30 or 45 days, but others provide coverage for longer trips.

See IMG's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Most plans may cover preexisting conditions under set parameters or up to specific amounts. For example, the iTravelInsured Travel LX travel insurance plan shown above may cover preexisting conditions if you purchase the insurance within 24 hours of making the final payment for your trip.

For the travel medical insurance plans shown above, preexisting conditions are covered for travelers younger than 70. However, coverage is capped based on your age and whether you have a primary health insurance policy.

- Some annual multi-trip plans are modestly priced.

- iTravelInsured Travel LX may offer optional cancel for any reason and interruption for any reason coverage, if eligible.

Purchase your policy here: IMG .

Travelex Insurance

Travelex offers three single-trip plans: Travel Basic, Travel Select and Travel America. However, only the Travel Basic and Travel Select plans would be applicable for my trip to Turkey.

See Travelex's COVID-19 coverage statement for coronavirus-specific information.

Typically, Travelex won't cover losses incurred because of a preexisting medical condition that existed within 60 days of the coverage effective date. However, the Travel Select plan may offer a preexisting condition exclusion waiver. To be eligible for this waiver, the insured traveler must meet all the following conditions:

- You purchase the plan within 15 days of the initial trip payment.

- The amount of coverage purchased equals all prepaid, nonrefundable payments or deposits applicable to the trip at the time of purchase. Additionally, you must insure the costs of any subsequent arrangements added to the same trip within 15 days of payment or deposit.

- All insured individuals are medically able to travel when they pay the plan cost.

- The trip cost does not exceed the maximum trip cost limit under trip cancellation as shown in the schedule per person (only applicable to trip cancellation, interruption and delay).

- Travelex's Travel Select policy can cover trips lasting up to 364 days, which is longer than many single-trip policies.

- Neither Travelex policy requires receipts for trip and baggage delay expenses less than $25.

- For emergency evacuation coverage, you or someone on your behalf must contact Travelex and have Travelex make all transportation arrangements in advance. However, both Travelex policies provide an option if you cannot contact Travelex: Travelex will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Travelex Insurance .

Seven Corners

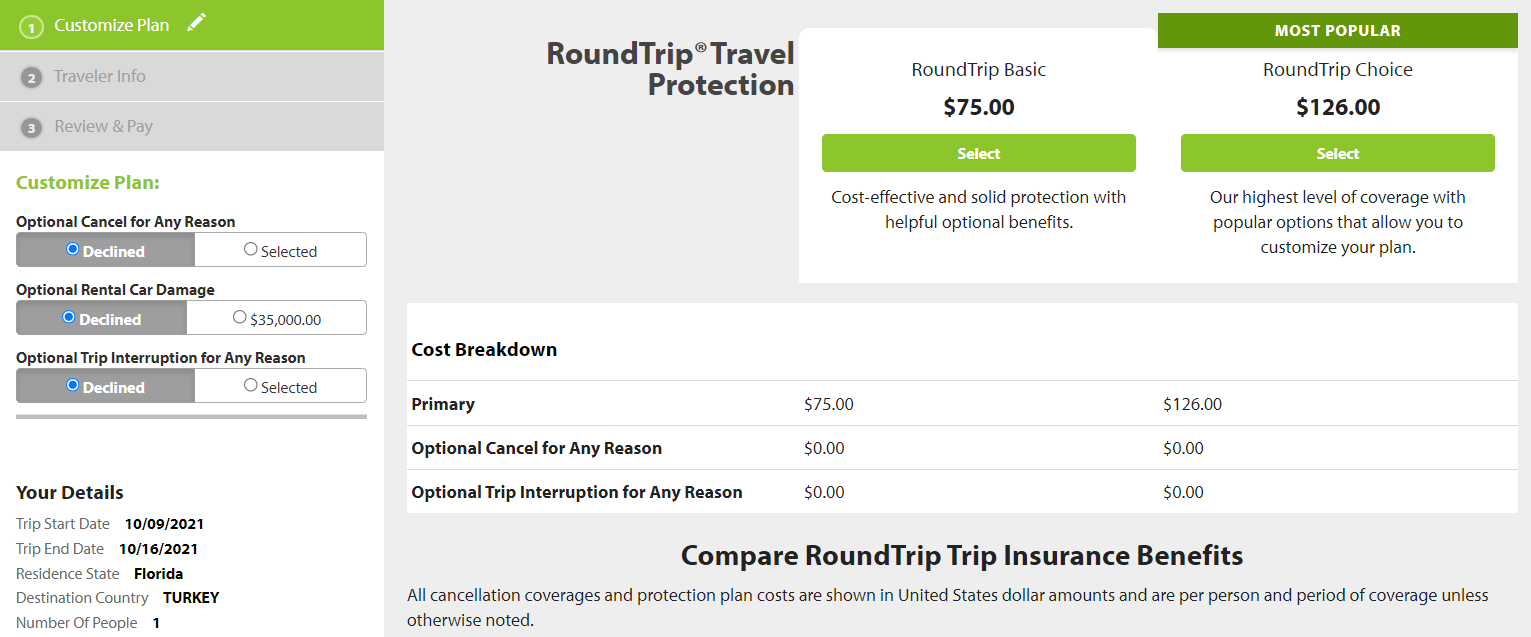

Seven Corners offers a wide variety of policies. Here are the policies that are most applicable to travelers on a single international trip.

Seven Corners also offers many other types of travel insurance, including an annual multi-trip plan. You can choose coverage for trips of up to 30, 45 or 60 days when purchasing an annual multi-trip plan.

See Seven Corner's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Typically, Seven Corners won't cover losses incurred because of a preexisting medical condition. However, the RoundTrip Choice plan offers a preexisting condition exclusion waiver. To be eligible for this waiver, you must meet all of the following conditions:

- You buy this plan within 20 days of making your initial trip payment or deposit.

- You or your travel companion are medically able and not disabled from travel when you pay for this plan or upgrade your plan.

- You update the coverage to include the additional cost of subsequent travel arrangements within 15 days of paying your travel supplier for them.

- Seven Corners offers the ability to purchase optional sports and golf equipment coverage. If purchased, this extra insurance will reimburse you for the cost of renting sports or golf equipment if yours is lost, stolen, damaged or delayed by a common carrier for six or more hours. However, Seven Corners must authorize the expenses in advance.

- You can add cancel for any reason coverage or trip interruption for any reason coverage to RoundTrip plans. Although some other providers offer cancel for any reason coverage, trip interruption for any reason coverage is less common.

- Seven Corners' RoundTrip Choice policy offers a political or security evacuation benefit that will transport you to the nearest safe place or your residence under specific conditions. You can also add optional event ticket registration fee protection to the RoundTrip Choice policy.

Purchase your policy here: Seven Corners .

World Nomads

World Nomads is popular with younger, active travelers because of its flexibility and adventure-activities coverage on the Explorer plan. Unlike many policies offered by other providers, you don't need to estimate prepaid costs when purchasing the insurance to have access to trip interruption and cancellation insurance.

World Nomads offers two single-trip plans.

World Nomads has a page dedicated to coronavirus coverage , so be sure to view it before buying a policy.

World Nomads won't cover losses incurred because of a preexisting medical condition (except emergency evacuation and repatriation of remains) that existed within 90 days of the coverage effective date. Unlike many other providers, World Nomads doesn't offer a waiver.

- World Nomads' policies cover more adventure sports than most providers, so activities such as bungee jumping are included. The Explorer policy covers almost any adventure sport, including skydiving, stunt flying and caving. So, if you partake in adventure sports while traveling, the Explorer policy may be a good fit.

- World Nomads' policies provide nonmedical evacuation coverage for transportation expenses if there is civil or political unrest in the country you are visiting. The coverage may also transport you home if there is an eligible natural disaster or a government expels you.

Purchase your policy here: World Nomads .

Other options for buying travel insurance

This guide details the policies of eight providers with the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip to search. Just note that these search engines won't show every policy and every provider, and you should still research the provided policies to ensure the coverage fits your trip and needs.

You can also purchase a plan through various membership associations, such as USAA, AAA or Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Should you get travel insurance if you have credit card protection?

Is travel insurance worth getting?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home . In that case, you should consider purchasing travel insurance. If you travel frequently, buying an annual multi-trip policy may be worth it.

What is the best COVID-19 travel insurance?

There are various aspects to keep in mind in the age of COVID-19. Consider booking travel plans that are fully refundable or have modest change or cancellation fees so you don't need to worry about whether your policy will cover trip cancellation. This is important since many standard comprehensive insurance policies won't reimburse your insured expenses in the event of cancellation if it's related to the fear of traveling due to COVID-19.

However, if you book a nonrefundable trip and want to maintain the ability to get reimbursed (up to 75% of your insured costs) if you choose to cancel, you should consider buying a comprehensive travel insurance policy and then adding optional cancel for any reason protection. Just note that this benefit is time-sensitive and has eligibility requirements, so not all travelers will qualify.

Providers will often require CFAR purchasers insure the entire dollar amount of their travels to receive the coverage. Also, many CFAR policies mandate that you must cancel your plans and notify all travel suppliers at least 48 hours before your scheduled departure.

Likewise, if your primary health insurance won't cover you while on your trip, it's essential to consider whether medical expenses related to COVID-19 treatment are covered. You may also want to consider a MedJet medical transport membership if your trip is to a covered destination for coronavirus-related evacuation.

Ultimately, the best pandemic travel insurance policy will depend on your trip details, travel concerns and your willingness to self-insure. Just be sure to thoroughly read and understand any terms or exclusions before purchasing.

What are the different types of travel insurance?

Whether you purchase a comprehensive travel insurance policy or rely on the protections offered by select credit cards, you may have access to the following types of coverage:

- Baggage delay protection may reimburse for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. Typically, you may be reimbursed up to a particular amount per incident or per day.

- Lost/damaged baggage protection may provide reimbursement to replace lost or damaged luggage and items inside that luggage. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and sometimes transportation when you're delayed for a substantial time while traveling on a common carrier such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may provide reimbursement if you need to cancel or interrupt your trip for a covered reason, such as a death in your family or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if deemed necessary by the insurance provider and a medical professional. This coverage can be particularly valuable if you're traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimburse you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to take the vehicle to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

Should I buy travel health insurance?

If you purchase travel with credit cards that provide various trip protections, you may not see much need for additional travel insurance. However, you may still wonder whether you should buy travel medical insurance.

If your primary health insurance covers you on your trip, you may not need travel health insurance. Your domestic policy may not cover you outside the U.S., though, so it's worth calling the number on your health insurance card if you have coverage questions. If your primary health insurance wouldn't cover you, it's likely worth purchasing travel medical insurance. After all, as you can see above, travel medical insurance is often very modestly priced.

How much does travel insurance cost?

Travel insurance costs depend on various factors, including the provider, the type of coverage, your trip cost, your destination, your age, your residency and how many travelers you want to insure. That said, a standard travel insurance plan will generally set you back somewhere between 4% and 10% of your total trip cost. However, this can get lower for more basic protections or become even higher if you include add-ons like cancel for any reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. Or, visit an insurance aggregator like InsureMyTrip to quickly compare options across multiple providers.

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like CFAR protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

However, many plans may still offer a preexisting conditions waiver for those who qualify if you buy your travel insurance within 14 to 21 days of your first trip expense or deposit (this time frame may vary by provider). If you don't need a preexisting conditions waiver or aren't interested in CFAR coverage, you can purchase travel insurance once your departure date nears.

You must purchase coverage before it's needed. Some travel medical plans are available for purchase after you have departed, but comprehensive plans that include medical coverage must be purchased before departing.

Additionally, you can't buy any medical coverage once you require medical attention. The same applies to all travel insurance coverage. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided upon the best travel insurance plan for your trip, you should be able to complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction is complete.

Related: 7 times your credit card's travel insurance might not cover you

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, read and understand the policy documents. By doing so, you can choose a plan that's appropriate for you and your trip — including the features that matter most to you.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't contain exclusions for these activities. Likewise, if you're making two back-to-back trips during which you'll be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

If you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.

Disclaimer : This information is provided by IMT Services, LLC ( InsureMyTrip.com ), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com .

- Search Search Please fill out this field.

What Is Travel Insurance?

Understanding travel insurance, how travel insurance works, comprehensive travel insurance.

- Trip Cancellation or Interruption

Damage and Baggage Losses Coverage

Rental insurance, travel health insurance.

- AD&D Coverage

Other Travel Insurance Coverage

How to get travel insurance, the bottom line.

- Personal Finance

What Is Travel Insurance, and What Does It Cover?

Julia Kagan is a financial/consumer journalist and former senior editor, personal finance, of Investopedia.

:max_bytes(150000):strip_icc():format(webp)/Julia_Kagan_BW_web_ready-4-4e918378cc90496d84ee23642957234b.jpg "house of travel insurance")

Jackyenjoyphotography / Getty Images

Travel insurance is a type of insurance covering financial losses associated with traveling, and it can be useful protection for domestic or international travel. Whether you missed your flight to Florida, lost your bags in Berlin, or broke your ankle in Ankara, the best travel insurance companies can help remedy all kinds of travel mishap costs.

Key Takeaways

- Travel insurance can be purchased online, from your tour operator, or from other sources.

- The main categories of travel insurance include trip cancellation or interruption coverage, baggage and personal effects coverage, rental property and rental car coverage, medical coverage, and accidental death coverage.

- Coverage often includes 24/7 emergency services, such as replacing lost passports, cash wire assistance, and rebooking canceled flights.

- It's important to understand what's covered and what's not, and any limitations on coverage amounts and coverage requirements.

Travel insurance helps cover financial losses associated with surprise circumstances that could ruin a trip, including illness, injury, accidents, flight or other transportation delays, and other issues. This insurance costs 4% to 10% of a trip's price. So, for a $10,000 trip, trip insurance could cost between $400 and $1,000.

Premiums—or the price you pay for coverage—are based on the coverage type, your age, destination, trip cost, and more. Specialized policy riders focus on the needs of business travelers, athletes, and expatriates .

You may already have travel insurance coverage from your homeowners or renters insurance or your credit cards. Call your insurance agent to find out about your current travel coverage, and your credit card company to find out about any benefits you get when you purchase air or train tickets, rent a car, or book a hotel using the card. Many travel rewards cards come with built-in travel insurance and other travel benefits.

Travel insurance may be sold online by travel agents, travel suppliers (airlines, cruise lines), private insurance companies, or insurance brokers when booking your flight, accommodations, or car. Travel insurance companies include AIG Travel, Berkshire Hathaway Travel Protection, Generali Global Assistance, GeoBlue, Nationwide, and more.

Typically, you'll purchase coverage shortly after initial bookings for lodging, flights, or other transportation, activities, and rental cars. Some policies may require you to do so to retain full coverage. Here are some terms to know for travel insurance.

Primary and Secondary Coverage

If you buy travel insurance, you may have concurrent insurance coverage , meaning you're covered under more than one policy. When the travel coverage is primary, the travel insurance reimburses you first without needing to make a claim through another company—and sparing you potentially increased policy rates.

If the travel insurance coverage is secondary, you'll first need to attempt to file a claim with other coverage, such as an airline (lost baggage) or your own auto insurance (damaged car).

Coverage Requirements

There are usually stipulations spelled out on how you qualify for coverage. Your claim must fall under the types of coverage offered. For example, lost baggage insurance might include coverage for personal items, prescriptions, credit cards, and your passport or visa. You may also need to take extra steps to qualify for coverage, such as reporting the loss or theft to the police.

Policy Coverage Limits

This is the maximum amount you can receive for the claim. For example, you might only receive $500 per bag. You may not even receive more for expensive items such as jewelry or electronic devices. You might need to provide receipts for items over a certain amount. Without receipts, the insurer may only pay for repairs.

Some coverage might require you to pay a deductible, or flat amount, before covering the remainder of your claim up to the limit.

These are the conditions under which your coverage will not cover the loss. Each policy differs. For example, your baggage damage coverage may not cover losses caused by animals. It may exclude coverage of bicycles, hearing aids or other medical devices, keys, and tickets, or seizure by a government or customs official.

Pre-existing conditions may not be covered by travel medical insurance, or may only be covered if you buy a travel insurance plan within one to two weeks of booking your trip.

Comprehensive travel insurance includes many types of coverage listed below, bundled into one plan. Most commonly, comprehensive travel insurance bundles a 24-hour assistance line to help find doctors or get assistance in an emergency, reimburse you for trip cancellation , interruption and delay, baggage loss or delay, and medical expense and medical evacuation coverage.

Alternatively, you can purchase each coverage type separately. This may be wise if you already have coverage through other insurance or can cover your losses in many cases.

Trip Cancellation or Interruption Coverage

This insurance reimburses a traveler for some or all prepaid, nonrefundable travel expenses, and comes in the following forms:

- Trip cancellation : Reimburses you for paid travel expenses if you can't travel for a preapproved reason.

- Travel delay : Reimburses you for expenses if you can't travel because of a delay.

- Trip interruption : Reimburses you for travel costs if your trip is cut short.

- Cancel for any reason (CFAR) : Reimburses you for a portion of costs if you cancel the trip for any reason; typically more expensive than the other types listed above.

With most of the above, acceptable cancellation and interruption causes and reimbursement amounts vary by provider. Acceptable reasons for a claim might include the following:

- Your illness

- Illness or death in your immediate family

- Sudden business conflicts

- Weather-related issues

- Legal obligations such as jury duty

You may need to pay more or meet more requirements to file a claim for a cancellation due to financial default, terrorism in your destination city, or work reasons.

When traveling, register your travel plans with the State Department through its free travel registration website , the Smart Traveler Enrollment Program (STEP). The nearest embassy or consulate can contact you if there is a family, state, or national emergency.

Baggage and personal belongings being lost, stolen, or damaged is a frequent travel problem—and can quickly ruin a trip as you must shop for replacements. Baggage and personal effects coverage protects lost, stolen, or damaged belongings during travel to, in, and from a destination.

However, many travel insurance policies pay for belongings only after you exhaust all other available claims. Baggage coverage may have many restrictions and exclusions, such as only covering up to $500 per item and $250 for each additional item. You may be able to increase or decrease amounts, shop around for coverage, or increase limits by paying more.

For example, the insurance may not pay for lost and damaged luggage due to airline fault. Most carriers, such as airlines, reimburse travelers if baggage is lost or destroyed due to the airline's error. However, there may be limitations on reimbursement amounts, so baggage and personal effects coverage provide an additional layer of protection.

Vacation rental insurance covers costs from accidental damage to a vacation rental property. Some plans also offer trip cancellation and interruption to help reimburse costs when you can't use your vacation rental. Some of these reasons could include the following:

- Lost or stolen keys

- Unsanitary or unsafe vacation property

- Vacation rental wasn't as advertised

- The company oversold your vacation rental

Rental car insurance covers a rental car's damage or loss while on a trip, taking the place of the rental agency's collision damage waiver (CDW) or your regular car insurance policy. Policies vary and may cover collisions, theft, vandalism, and other incidents. Rental car insurance may be a secondary policy to your own car insurance. However, it doesn't cover your liability or legal responsibility for damage or injury you cause to others.

Medical coverage can help with unexpected international medical and dental expenses, and help with locating doctors and healthcare facilities abroad. As with other policies, coverage will vary by price and provider.

- Foreign travel medical coverage : These policies range from five days to one year or longer, and cover costs arising from illness and injuries while traveling.

- Medical evacuation: May cover airlift travel to a medical facility and medical evacuation to receive care.

Consult with your current medical insurers before purchasing a policy to determine whether a policy extends its coverage outside the country. Most health insurance companies pay “customary and reasonable” hospital costs if you become sick or injured while traveling, but few will pay for a medical evacuation.

The U.S. government doesn't insure citizens or pay for medical expenses abroad . Before purchasing a policy, read the provisions to see what exclusions, such as preexisting medical conditions, apply. Don't assume that the new coverage mirrors that of your existing plan. Routine medical care is typically excluded unless you buy a long-term medical plan intended for expatriates, missionaries, maritime crew members, or others abroad for extended periods.

Medicare or Medicaid generally don't cover medical costs overseas unless you have specific Medicare Advantage or Medigap plans covering emergency overseas care.

Accidental Death and Dismembership (AD&D) Coverage

If an accident results in death or serious injury, an AD&D policy pays a lump sum to surviving beneficiaries or you for an injury. The insurance usually offers three parts, providing coverage for accidents and fatalities:

- Flight accident insurance: Occurring during flights on a licensed commercial airliner.

- Common carrier: Resulting from public transportation such as train, ferry, or bus travel.

- General travel: Occurring at any point during a trip.

Exclusions that may apply include death caused by drug overdose or sickness. In addition, only some injuries may be covered, specifically hand, foot, limb, or eyesight. There are stated amount limits per injury.

Accidental death coverage may not be necessary if you already have a life insurance policy. However, benefits paid by your travel insurance coverage may be in addition to those paid by your life insurance policy, leaving more money to your beneficiaries.

Depending on your plan or package selected, you may be able to add the following travel insurance types:

- Identity theft resolution services

- School activity coverage

- Destination wedding coverage

- Adventure sports coverage

- Pet health as a reason for cancellation or delay

- Hunting or fishing activities as a reason for cancellation or delay

- Missed flight connections

Travel insurance varies in cost, exclusions, and coverage. Coverage is available for single, multiple, and yearly trips. To get travel insurance, you fill out an insurance company's application about your trip, including the following:

- Travelers going

- Destination

- Travel dates

- Date of first payment toward your trip

The insurance company reviews the information using underwriting guidelines to guide issuing a policy and the rate. If it accepts your application, the company will issue a policy covering your trip. If the company rejects your application, you can apply with another insurer.

When you receive your policy, you'll typically get a 10- to 15-day review period to review the contract's fine details. If you don't like the policy, you can return it for a refund. Read through the document and ensure the plan you purchased doesn't apply too many loopholes, and that it covers:

- Emergency medical care and transport back to the U.S.

- High enough limits to cover your costs or damages

- Regions you're traveling to

- Your trip duration or number of trips

- All activities you plan to enjoy

- Preexisting conditions and people of your age

Also, read through for any exclusions. For example, types of property covered, and whether property lost or damaged by the airline is covered, and how.

Do I Need Travel Insurance?

You might consider travel insurance if you can't afford to cancel and then rebook an expensive or long trip. You might also consider travel health insurance if your health insurance doesn't cover international costs. An alternative is to book an easily cancellable vacation—look for a pay-later hotel room and car rental options, flexible cancellation terms, and the ability to rebook without a fee.

What Is Not Covered by Travel Insurance?

Review the travel insurance policy to discover exclusions. According to NAIC, common travel policy exclusions are:

- A traveler's pre-existing health conditions

- Civil and political unrest at the traveler's destination

- Pregnancy and childbirth

- Coverage for those engaging in adventure or dangerous activities.

Pandemics may also be excluded from coverage.

How Can I Get Cheap Travel Insurance?

Your homeowners or renters insurance may provide some protection for personal belongings, and airlines and cruise lines are responsible for loss and damage to your baggage during transport. Also, credit cards may provide automatic protection for things like delays and luggage or rental car accidents if used for deposits or other trip-related expenses.

The main types of travel insurance include trip cancellation or interruption coverage, baggage and personal effects coverage, medical expense coverage, and accidental death or flight accident coverage. Before buying a policy, check to see if you already have coverage through your own health or car insurance or a credit card.

Mass.gov. " Travel Insurance. "

Minnesota Department of Commerce. " Travel Insurance ."

U.S. Travel Insurance Association. " Frequently Asked Questions ."

Texas Department of Insurance. " Should You Get Travel Insurance? "

National Association of Insurance Commissioners. “ Taking a Trip? Information about Travel Insurance You Should Know Before You Hit the Road .”

U.S. Department of State. “ Your Health Abroad. ”

Medicare.gov. " Medicare Coverage Outside the United States ." Page 4.

Medicare.gov. " Medigap & Travel. "

NAIC. " Travel Insurance ."

:max_bytes(150000):strip_icc():format(webp)/Primary-Image-how-much-does-travel-insurance-cost-7377124-c44e95776d284d3e84b756908efb5add.jpg "house of travel insurance")

- Terms of Service

- Editorial Policy

- Privacy Policy

- Your Privacy Choices

Sleepover at Polly Pocket's? How to stay in the iconic '90's compact-themed Airbnb

Spending the night in Polly Pocket's bright and colorful world has never been easier.

To celebrate Polly Pocket's 35th birthday, the Mattel -owned toy has created an Airbnb in the iconic '90s Polly Pocket compact style. The two-story " Slumber Party Fun " compact features a vanity full of hair and nail accessories, a retro fridge, Polly Pocket's closet, a friendship bracelet-making station, and a life-sized Action Park Tent 10 feet away from the compact.

"Try on my most iconic outfits—yes, the ones you used to chew on when you were younger—in my closet," the Airbnb listing reads, a humorous nod to the very chewable rubber clothes that were used to dress Polly Pocket. "They slip on right over your clothes and are extremely chic. No bite marks, please!"

Polly Pocket is the host of the Airbnb , according to the listing.

Meet the 'Dream Besties': Barbie-launched dolls that have goals like owning a tech company

How to book the Polly Pocket Airbnb

The Airbnb is located in Littleton, Massachusetts, and is available for guests to book starting Aug. 21 at 6 a.m. PT (9 a.m. ET) through Aug. 28 at 11:59 p.m. PT (2:59 a.m. ET) for one of three one-night stays happening Sept. 12-14.

The Airbnb can sleep four guests each in the adjacent tent and will cost $89 a person, symbolic of Polly Pocket's 1989 debut.

According to a release, Polly Pocket is also opening the location for 21 daytime experiences for up to 12 guests during from Sept. 16 to Oct. 6. Those can be booked starting Sug. 21 at 6 a.m. PT (9 a.m. ET) through Aug. 28 at 11:59 p.m. PT (2:29 a.m. ET).

Any guests visiting the Airbnb are responsible for their own travel to and from Littleton, which is located about 40 miles west of Boston.

See photos of Polly Pocket's Airbnb

Advertisement

Supported by

Fact-Checking Claims About Tim Walz’s Record

Republicans have leveled inaccurate or misleading attacks on Mr. Walz’s response to protests in the summer of 2020, his positions on immigration and his role in the redesign of Minnesota’s flag.

- Share full article

By Linda Qiu

Since Gov. Tim Walz of Minnesota was announced as the Democratic nominee for vice president, the Trump campaign and its allies have gone on the attack.

Mr. Walz, a former teacher and football coach from Nebraska who served in the National Guard, was elected to the U.S. House of Representatives in 2006 and then as Minnesota’s governor in 2018. His branding of former President Donald J. Trump as “weird” this year caught on among Democrats and helped catapult him into the national spotlight and to the top of Vice President Kamala Harris’s list of potential running mates.

The Republican accusations, which include questions over his military service , seem intended at undercutting a re-energized campaign after President Biden stepped aside and Ms. Harris emerged as his replacement at the top of the ticket. Mr. Trump and his allies have criticized, sometimes inaccurately, Mr. Walz’s handling of protests in his state, his immigration policies, his comments about a ladder factory and the redesign of his state’s flag.

Here’s a fact check of some claims.

What Was Said

“Because if we remember the rioting in the summer of 2020, Tim Walz was the guy who let rioters burn down Minneapolis.” — Senator JD Vance of Ohio, the Republican nominee for vice president, during a rally on Wednesday in Philadelphia

This is exaggerated. Mr. Walz has faced criticism for not quickly activating the National Guard to quell civil unrest in Minneapolis in the summer of 2020 after the murder of George Floyd by a police officer. But claims that he did not respond at all, or that the city burned down, are hyperbolic.

Mr. Floyd was murdered on May 25, 2020, and demonstrators took to the streets the next day . The protests intensified, with some vandalizing vehicles and setting fires. More than 700 state troopers and officers with the Minnesota Department of Natural Resources’ mobile response team were deployed on May 26 to help the city’s police officers, according to a 2022 independent assessment by the state’s Department of Public Safety of the response to the unrest.

But the report noted that issues with communication delayed the deployment of the state National Guard.

The mayor, Jacob Frey, asked Mr. Walz to activate the National Guard the night of May 27. An aide to Mr. Frey texted a colleague around 8 p.m. that Mr. Walz was “hesitating,” documents obtained by the local news media show . The Trump campaign cited these records as evidence of Mr. Walz’s refusal to act.

Mr. Walz has argued that he did not believe Mr. Frey “knew what he was asking for,” and that the mayor did not specify the number of troops, their mission or their abilities.

The city’s police department submitted a written request the night of May 27 for 600 guardsmen. State officials said that the request was not specific enough and that they were waiting for more detail before approving the request, but that city officials were not aware that more detail was needed, according to the 2022 report.

Mr. Frey sent a formal request for troops the morning of May 28, and Mr. Walz activated the National Guard shortly afterward — two days after protests had begun. The Guard tweeted at about 4 p.m. local time that it was ready to respond to the governor’s request.

By that time, one of the city’s police precincts had already been damaged by fire. The Trump campaign also noted that a police officer testified in 2020 that she had heard “thirdhand” that Mr. Walz had said to “give up the precinct”; at the time, a spokesman for Mr. Walz disputed that characterization.

It is also worth noting that Mr. Trump, in a June 2020 phone call with governors, praised Mr. Walz’s response: “Tim Walz. Again, I was very happy with the last couple of days, Tim. You called up big numbers and the big numbers knocked them out so fast.”

“I know him a little bit. I helped him during the riots because his house was surrounded by people that were waving an American flag — doesn’t sound like very bad people. He called me and he was very concerned, very, very concerned that it was going to get out of control. They only had one guard, I guess, it was at the mansion or his house in some form. And he called me. And I said what do you want me to do about it? I was in the White House. He said if you would put out the word that I’m a good person. And I did. I put out the word.” — Mr. Trump in an interview on Fox News on Wednesday

This is misleading. Mr. Trump’s version of events is wrong on several details, and Mr. Walz’s own account noticeably differs.

On April 17, 2020 — more than a month before George Floyd’s murder — hundreds of demonstrators gathered in front of Mr. Walz’s residence to protest a stay-at-home order the governor had imposed because of the coronavirus pandemic.

That morning, Mr. Trump had written on social media, “LIBERATE MINNESOTA!,” along with calls to “liberate” other states under lockdown orders.

That day, Mr. Walz said he had tried unsuccessfully to call Mr. Trump and Vice President Mike Pence to ask “what they think we could have done differently” to respond to the spread of the virus.

Three days later, on April 20, Mr. Trump wrote that he had received a “very nice call” from Mr. Walz and that “good things are happening.”

In a news conference that day, Mr. Walz said that he had a “very good and long conversation” with Mr. Trump on April 18 — after the protesters had left — about the need for more personal protective equipment and testing abilities.

In an interview with Politico in September 2021 published this week, Mr. Walz said that Mr. Trump’s tweet had “brought armed people to my house” and that Mr. Trump had never responded when he asked what “liberate Minnesota” meant.

“Tim Walz went on TV to talk about trying to help illegal aliens climb over the border wall. Tim Walz championed government-issued IDs, driver’s licenses for illegal aliens, which results in countless motorists being killed each and every year. Tim Walz championed free health care for illegal aliens, which will bankrupt America.” — Stephen Miller, a former Trump administration official, in an interview on Fox News on Tuesday

This is exaggerated. Mr. Miller distorted comments Mr. Walz made regarding a border wall. He is correct that Mr. Walz signed legislation allowing unauthorized immigrants to obtain driver’s licenses and giving them publicly subsidized health care coverage through a state program for low-income individuals. But while Mr. Walz championed eligibility expansion, it is unclear whether he supported the health care expansion.

In 2023, Mr. Walz signed legislation expanding driver’s license eligibility to all residents of the state, regardless of immigration status. In a news release , he said he was a “longtime supporter of the bill” and expressed pride at the measure, saying it would make roads safer.

That May, Mr. Walz also signed a budget deal into law that, among other provisions, allowed unauthorized immigrants to enroll in MinnesotaCare , the state’s program for low-income residents. Mr. Walz’s budget had proposed expanding eligibility only to undocumented immigrants under 19, and a local publication reported that he opposed allowing undocumented adults to also have access to the program. His news release at the time did not mention the expansion. Additionally, MinnesotaCare provides subsidized, but not always free insurance. The health care program is funded in part by the state, and the expansion, backed by state money , would not dip into federal coffers and “bankrupt” the country.

Mr. Miller’s comment about Mr. Walz helping immigrants “climb over the border wall” distorts Mr. Walz’s remarks. In an interview last week on CNN , Mr. Walz said that the “United States needs to control its border” but argued that Mr. Trump was “not interested in solving the problem.”

“I always say, let me know how high it is,” he said, wryly expressing the ineffectiveness of a border wall. “If it’s 25 feet, then I’ll invest in the 30-foot ladder factory. That’s not how you stop this.”

He continued, “You stop this using electronics, you stop it using more border control agents, and you stop it by having a legal system that allows for that tradition of allowing folks to come here, just like my relatives did to come here, be able to work and establish the American dream. He’s not interested in that. He wants to demonize.”

“Don’t forget he tried to redesign the Minnesota state flag to look like the Somali national flag. You just can’t get further out there in America.” — Representative Andy Biggs, Republican of Arizona, in an interview on a right-wing streaming platform on Wednesday

False. Minnesota adopted a new flag on May 11, after a monthslong redesign effort and thousands of public submissions. Mr. Walz had little to do with the design, which pays tribute to various facets of the state — not Somalia.

Prompted by criticism that the state’s old flag was offensive to Native Americans and bore too many similarities to other state flags, Minnesota legislators passed a measure in 2023 establishing a commission to redesign the state’s emblems. Mr. Walz signed that legislation into law. The commission received more than 2,000 submissions from the public through October 2023 and decided on a design in December.

The commission — not Mr. Walz — chose and modified a design by Andrew Prekker of Luverne, Minn. Mr. Prekker, who does part-time work in graphic design, said in an interview on local news that he had researched his concept and tried to create imagery that “represented everyone” in the state. Mr. Prekker told PolitiFact that his flag had nothing to do with Somalia.

The new flag has a white eight-point star (representing the North Star, which is the state’s motto, and the many cultures of the state) splashed on a dark blue background (representing the night sky and the shape of the state) on the left and a bright blue field on the right (representing the state’s 11,000 lakes and 6,000 rivers and streams), according to the commission’s final report.

The flag of Somalia features a white five-pointed star on a blue field.

An earlier version of this article misidentified a Minnesota agency that deployed a mobile response team to help quell unrest in Minneapolis after the murder of George Floyd by a police officer. It was the Minnesota Department of Natural Resources, not the Department of National Resources.

An earlier version of this article misstated the damage to one of Minneapolis’s police precincts. It was damaged by fire but not burned to the ground.

How we handle corrections

Linda Qiu is a reporter who specializes in fact-checking statements made by politicians and public figures. She has been reporting and fact-checking public figures for nearly a decade. More about Linda Qiu

Keep Up With the 2024 Election

The presidential election is 80 days away . Here’s our guide to the run-up to Election Day.

Tracking the Polls . The state of the race, according to the latest polling data.

Election Calendar. Take a look at key dates and voting deadlines.

Swing State Ratings. The presidential race is likely to be decided by these states.

Candidates’ Careers. How Trump, Vance, Harris and Walz got here.

Harris on the Issues. Where Harris stands on immigration, abortion and more.

Trump’s 2025 Plans. Trump is preparing to radically reshape the government.

Money blog: Couples reveal how they split finances when one earns more than other

Welcome to the Money, your place for personal finance and consumer news and tips. Read our weekend feature on relationship finances below and let us know how you and your partner divide money in the comments box. We'll be back with live updates on Monday.

Saturday 17 August 2024 12:43, UK

Essential reads

- Couples on how they split finances when one earns more than other

- What's gone wrong at Asda?

- The week in money

- Best of the Money blog - an archive of features

Tips and advice

- All discounts you get as student or young person

- Save up to half price on top attractions with this trick

- Fines for parents taking kids out of school increasing next month

- TV chef picks best cheap eats in London

- 'I cancelled swimming with plenty of notice - can they keep my money?'

Ask a question or make a comment

By Emily Mee , news reporter

Openly discussing how you split your finances with your partner feels pretty taboo - even among friends.

As a consequence, it can be difficult to know how to approach these conversations with our partner or what is largely considered fair - especially if there's a big imbalance salary-wise.

Research by Hargreaves Lansdown suggests in an average household with a couple, three-quarters of the income is earned by one person.

Even when there is a large disparity, some couples will want to pay the same amount on bills as they want to contribute equally.

But for others, one partner can feel resentful if they are spending all of their money on bills while the other has much more to spend and is living a different lifestyle as a result.

At what stage of the relationship can you talk about money?

"We've kind of formally agreed there is some point in a relationship you start talking about kids - there is no generally agreed time that we start talking about money," says Sarah Coles, head of personal finance at Hargreaves Lansdown.

Some couples may never get around to mentioning it, leading to "lopsided finances".

Ms Coles says if you want to keep on top of finances with your partner, you could set a specific date in the year that you go through it all.

"If it's in the diary and it's not emotional and it's not personal then you can properly go through it," she says.

"It's not a question of 'you need to pull more weight'. It's purely just this is what we've agreed, this is the maths and this is how we need to do that."

While many people start talking about finances around Christmas, Ms Coles suggests this can be a "trying time" for couples so February might be a "less emotional time to sit down".

How do you have the conversation if you feel the current arrangement is unfair?

Relationship counsellor at Relate , Peter Saddington, says that setting out the balance as "unfair" shouldn't be your starting point.

You need to be honest about your position, he says, but your conversation should be negotiating as a couple what works for both of you.

Before you have to jump into the conversation, think about:

- Letting your partner know in advance rather than springing it on them;

- Making sure you and your partner haven't drunk alcohol before having the conversation, as this can make it easy for it to spiral;

- Having all the facts to hand, so you know exactly how much you are spending;

- Using 'I' statements rather than 'you'. For example, you could say to your partner: "I'm really worried about my finances and I would like to sit down and talk about how we manage it. Can we plan a time when we can sit down and do it?"

Mr Saddington says if your partner is not willing to help, you should look at the reasons or question if there are other things in the relationship that need sorting out.

If you're having repeated arguments about money, he says you might have opposite communication styles causing you to "keep headbutting".

Another reason could be there is a "big resentment" lurking in the background - and it may be that you need a third party such as a counsellor, therapist or mediator to help resolve it.

Mr Saddington says there needs to be a "safe space" to have these conversations, and that a third party can help untangle resentments from what is happening now.

He also suggests considering both of your attitudes to money, which he says can be formed by your early life and your family.

"If you grew up in a family where there wasn't any money, or it wasn't talked about, or it was pushed that you save instead of spend, and the other person had the opposite, you can see where those conversations go horribly wrong.

"Understanding what influences each of you when it comes to money is important to do before you have significant conversations about it."

What are the different ways you can split your finances?

There's no one-size-fits-all approach, but there are several ways you can do it - with Money blog readers getting in touch to let us know their approach...

1. Separate personal accounts - both pay the same amount into a joint account regardless of income

Paul Fuller, 40, earns approximately £40,000 a year while his wife earns about £70,000.

They each have separate accounts, including savings accounts, but they pay the same amount (£900) each a month into a joint account to pay for their bills.

Paul says this pays for the things they both benefit from or have a responsibility for, but when it comes to other spending his wife should be able to spend as she likes.

"It's not for me to turn around to my wife and expect her to justify why she thinks it's appropriate to spend £150 in a hairdresser. She works her backside off and she has a very stressful job," he says.

However, their arrangement is still flexible. Their mortgage is going up by £350 a month soon, so his wife has agreed to pay £200 of that.

And if his wife wants a takeaway but he can't afford to pay for it, she'll say it's on her.

"Where a lot of people go wrong is being unable to have those conversations," says Paul.

2. Separate personal accounts - whoever earns the most puts more into a joint account

This is a more formal arrangement than the hybrid approach Paul and his wife use, and many Money blog readers seem to do this in one form or another judging by our inbox.

There's no right or wrong way to do the maths - you could both put in the same percentage of your individual salaries, or come up with a figure you think is fair, or ensure you're both left with the same amount of spending money after each payday.

3. Everything is shared

Gordon Hurd and his wife Brenda live by their spreadsheet.

Brenda earns about £800 more a month as she is working full-time while Gordon is freelance. Previously Gordon had been the breadwinner - so it's a big turnaround.

They each have separate accounts with different banks, but they can both access the two accounts.

How much is left in each account - and their incomings and outgoings - is all detailed in the spreadsheet, which is managed weekly.

Whenever they need to buy something, they can see how much is left in each account and pay from either one.

Gordon says this means "everyone knows how much is available" and "each person's money belongs to the other".

"We have never in the last decade had a single disagreement about money and that is because of this strategy," he says.

Money blog reader Shredder79 got in touch to say he takes a similar approach.

"I earn £50k and my wife earns just under £150k. We have one joint bank account that our wages go into and all our outgoings come out of. Some friends can't get their head around that but it's normal for us."

Another reader, Curtis, also puts his wages into a joint account with his wife.

"After all, when you have a family (three kids) it shouldn't matter who earns more or less!" he says.

Reader Alec goes further and says he questions "the authenticity of any long-term relationship or the certainly of a marriage if a couple does not completely share a bank account for all earnings and all outgoings".

"As for earning significantly more than the other, so what? If you are one couple or long-term partnership you are one team and you simply communicate and share everything," he says.

"Personally I couldn't imagine doing it any other way and I do instinctively wonder what issues or insecurities, whether it be in trust or something else, sit beneath the need to feel like you need to keep your finances separate from one another, especially if you are a married couple."

A reader going by the name lljdc agrees, saying: "I earn half of what my husband does because I work part-time. Neither of us has a solo account. We have one joint account and everything goes into this and we just spend it however we like. All bills come out of this too. Sometimes I spend more, sometimes he spends more."

4. Separate accounts - but the higher earner pays their partner an 'allowance'

If one partner is earning much more than the other, or one partner isn't earning for whatever reason, they could keep separate accounts and have the higher earner pay their partner an allowance.

This would see them transfer an agreed amount each week or month to their partner's account.

Let us know how you and your partner talk about and split finances in the comments box - we'll feature some of the best next week

By Jimmy Rice, Money blog editor

The centre-point of a significant week in the economy was inflation data, released first thing on Wednesday, that showed price rises accelerated in July to 2.2%.

Economists attributed part of the rise to energy prices - which have fallen this year, but at a much slower rate than they did last year.

As our business correspondent Paul Kelso pointed out, it felt like the kind of mild fluctuation we can probably expect month to month now that sky high price hikes are behind us, though analysts do expect inflation to tick up further through the remainder of the year...

Underneath the bonnet, service inflation, taking in restaurants and hotels, dropped from 5.7% to 5.2%.

This is important because a large part of this is wages - and they've been a concern for the Bank of England as they plot a route for interest rates.

On Tuesday we learned average weekly earnings had also fallen - from 5.7% to 5.4% in the latest statistics.

High wages can be inflationary (1/ people have more to spend, 2/ employers might raise prices to cover staff costs), so any easing will only aid the case for a less restrictive monetary policy. Or, to put it in words most people use, the case for interest rate cuts.

Markets think there'll be two more cuts this year - nothing has changed there.

Away from the economy, official data also illustrated the pain being felt by renters across the UK.

The ONS said:

- Average UK private rents increased by 8.6% in the 12 months to July 2024, unchanged from in the 12 months to June 2024;

- Average rents increased to £1,319 (8.6%) in England, £748 (7.9%) in Wales, and £965 (8.2%) in Scotland;

- In Northern Ireland, average rents increased by 10% in the 12 months to May 2024;

- In England, rents inflation was highest in London (9.7%) and lowest in the North East (6.1%).

Yesterday, we found the UK economy grew 0.6% over three months to the end of June.

That growth rate was the second highest among the G7 group of industrialised nations - only the United States performed better with 0.7%, though Japan and Germany have yet to released their latest data.

Interestingly, there was no growth at all in June, the Office for National Statistics said, as businesses delayed purchases until after the general election.

"In a range of industries across the economy, businesses stated that customers were delaying placing orders until the outcome of the election was known," the ONS said.

Finally, a shout for this analysis from business presenter Ian King examining what's gone wrong at Asda. It's been one of our most read articles this week and is well worth five minutes of your Friday commute or weekend...

We're signing out of regular updates now until Monday - but do check out our weekend read from 8am on Saturday. This week we're examining how couples who earn different amounts split their finances.

Each week we feature comments from Money blog readers on the story or stories that elicited most correspondence.

Our weekend probe into the myriad reasons for pub closures in the UK prompted hundreds of comments.

Landlords and campaigners, researchers and residents revealed to Sky News the "thousand cuts" killing Britain's boozers - and what it takes to survive the assault.

Here was your take on the subject...

I've been a publican for 19 years. This article is bang on! It's like you've overheard my conversations with my customers - COVID, cost of living, wages - the traditional British boozer going out of fashion. (My place: no food, no small children). Hey Jood

I own a small craft ale bar or micropub as some say. The current climate is sickening for the whole hospitality sector. This summer has been ridiculously quiet compared to previous ones. Micropubs were on the rise pre-COVID, but not now even we're struggling to survive… Lauren

I am an ex-landlord. It's ridiculous you can buy 10 cans for £10 or one pint for £5 now. It's not rocket science, it's a no-brainer: reverse the situation. Make supermarket beer more expensive than pub beer, then people will start to go out and mix again rather than getting drunk at home. Ivanlordpeers

Bought four pints of my regular drink at a supermarket for less than one pint in our local pub. It's becoming a luxury to go to a pub these days. Torquay David

Traditional pubs are being taken over by conglomerates who don't sell traditional beer, only very expensive lager, usually foreign, and other similar gassy drinks. How can they be called traditional pubs? Bronzestraw

The main reason for pubs closing is twofold! 1: The out-of-reach rents that the big groups charge landlords. 2: Landlords are told what stock they can hold and restrict where they can purchase it from. Strange, but most pubs belonged to the same groups! A pub-goer

Less pubs are managed now, pub companies are changing them to managed partnerships, putting the pressure onto inexperienced young ex-managers. Locals complain that their local pub has gone. but they don't use them enough. Can government regulate rents and beer prices for business owners? John Darkins

I was a brewery tenant in Scotland for many years and sequestrated because of the constant grabbing at my money by greedy brewers who wanted more and more. I made my pub very successful and was penalised by the brewery. James MacQuarrie

The only reason pubs are closing is locals only use them on Boxing Day, New Year's Eve, and one Sunday a year. Plus breweries don't need pubs, they sell enough through supermarkets! Use them or lose them. Peter Smith

The closing of pubs is a terrible shame. I still go to my local and have great memories of getting drunk in many in my hometown. They are important places in society. As someone once said: "No good story ever started with a salad." Kev K

It's the taxman killing pubs. £1 of every £3 sold. Utter disgrace. Stef

I go with my girlfriend, Prue, every day to my local. It's a shame what's happening to prices. It used to be full of people and joy but now it's a ghost town in the pub since prices are too high now. I wish we could turn back time and find out what went wrong. Niall Benson

Minimum wage is around £11 and the tax threshold is £12,600 per year. How can you possibly afford a night in a pub out when a pint costs between £3 and £8 a pint on those wages? Allan7777blue

Unfortunately, the very people who have kept these establishments going over the years (the working man) have been priced out, and they're paying the price. Dandexter