Cookies on GOV.UK

We use some essential cookies to make this website work.

We’d like to set additional cookies to understand how you use GOV.UK, remember your settings and improve government services.

We also use cookies set by other sites to help us deliver content from their services.

You have accepted additional cookies. You can change your cookie settings at any time.

You have rejected additional cookies. You can change your cookie settings at any time.

Beta This part of GOV.UK is being rebuilt – find out what beta means

VAT Transport

Vtrans021100 - zero-rating of passenger transport: transport of vehicles on ships, aircraft or trains - passengers or freight.

If vehicles are transported or ferried on ships, aircraft or trains, the supply by the operator will be either one of passenger or freight transport.

The carriage of a bus, coach or taxi with passengers is regarded as passenger transport, whether or not charged at the private car rate by the operator, and is zero-rated provided the supply would otherwise qualify for zero-rating under Group 8.

The transportation of unaccompanied vehicles, including buses and coaches, and trailers, at whatever rate charged, is treated as a supply of freight transport, and is not normally zero-rated (but see below).

The treatment of a supply in respect of all other vehicles is based on the rate charged as illustrated below.

Passenger transport

The transport of:

- vehicles with drivers or passengers charged under the private car rate, including motorcycles, cars, caravans and trailers;

- small commercial vehicles charged under the private car rate whether carrying passengers or freight.

Supplies of these services are treated as passenger transport and are zero-rated under Group 8, item 4(a).

Top of page

Freight transport

- vehicles charged at a rate appropriate to driver accompanied vans, lorries, buses and coaches (without passengers);

- drivers accompanying such vehicles;

- all unaccompanied vehicles and trailers whatever the rate charged.

Is this page useful?

- Yes this page is useful

- No this page is not useful

Help us improve GOV.UK

Don’t include personal or financial information like your National Insurance number or credit card details.

To help us improve GOV.UK, we’d like to know more about your visit today. Please fill in this survey (opens in a new tab) .

0208 561 2112 (London) 0131 333 2700 (Edinburgh)

Quick Quote

- Private hire

- Corporate hire

- Tour operators

- Schools and colleges

- Contract hire

- Contingency hire

- Dedicated staff travel service

- 36-seat Coach Hire

- 53-seat Coaches

- West London

- Coach servicing

- Why choose us

- Our London team

- Our Edinburgh team

- Customer charter

- Environment

- Accreditations

- Driver training

- Areas Covered

Is there VAT on coach travel?

We commonly hear the term VAT being thrown around throughout daily life, whether we be at work, doing our weekly shop or out in public, but what is VAT and when does it apply?

What is VAT?

Value Added Tax (VAT) is added to the majority of goods, products and services throughout the European Union and the United Kingdom at a value of 20%. This 20% then gets submitted to the government as a form of tax. However, there are a minority of goods and public services which are exempt from VAT, and others that are listed as zero-rated.

What is the difference between exempt and zero-rated?

Exempt and zero-rated are preferential statuses given by the government for certain essential goods and services.

Companies who supply zero-rated products are still able to reclaim their input VAT, even though they don’t add value added tax to their goods. This is because the product is still taxable, but the rate is 0%.

Companies who supply services and goods which are listed as exempt are not VAT registered. There is no value of VAT added to these products and so there is nothing to reclaim.

Coach travel is listed as a zero-rated essential service, meaning that there should be no VAT charge when travelling via coach. However, additional extras, such as catering or entertainment services in action whilst on board are VAT registered and you will be expected to pay the additional charge of 20% for these services. This is the same amongst all other forms of domestic passenger transport which can be used to carry 10 or more people at a time.

If you would like to find out more about the costs of coach travel with City Circle , get in touch with our friendly bookings team who will be happy to assist and advise you in regard to any future bookings. Whether you are based in the UK or Scotland, we have a happy and helpful team waiting to assist you with any coach travel queries. Call our London branch on 020 8561 2112 or our Edinburgh branch on 0131 333 2700 . You can also email us at [email protected] and we will respond to your query within 24 hours.

Contact City Circle

Contact City Circle and discuss your requirements with our team to shape your perfect journey.

0208 561 2112

0131 333 2700

The Pleo Blog

Looking for pleo.io ?

Tools & Tips

Is there VAT on train tickets? Don’t get derailed by hidden costs

Is there VAT on train tickets? Like all of life’s great questions, the answer is not as simple as it first appears. Value Added Tax rates on expenses such as train tickets and train travel is usually zero percent.

But there’s a big difference between zero-rated and being exempt from VAT taxation.

Keep reading to learn more about Value Added Tax on train travel, other forms of public transportation and how to account for VAT .

Content overview

Are train tickets subject to VAT in the UK?

Is there vat on public transportation in the uk, is there vat on other forms of transportation in the uk, how do vat refunds work for travel expenses, how to account for vat, pleo and train tickets a match made in heaven .

Train tickets in the UK fall under the zero-rated category. This means as a business you need to keep track of the 0% VAT you��’re paying on train travel in your VAT returns.

This is different from being exempt from VAT. Unlike exempt items, like postage stamps , which the government considers as entirely outside the scope of VAT. The advantage of zero rating is that businesses can claim back VAT on related purchases, benefiting their cash flow , without having to charge their customers extra.

Reclaiming VAT on zero-rated supplies is what makes zero percent VAT such a favourable tax rate. You can claim all the benefits without the drawback of charging your customers extra.

Domestic UK transport is usually 0% VAT so long as the vehicle, ship or aircraft has at least ten seats, including those for the driver and crew.

This might look like:

- Pleasure cruises

- Cliff lifts

- Excursions by coach or train (including steam railways)

- Horse-drawn buses

- Mystery coach or boat trips

- Sightseeing tours

- The transport element of park-and-ride schemes designed to reduce traffic congestion in city centres

But there are some exceptions to this rule, which often focus on whether the transport you’re supplying is to an event, experience or entertainment that you also own. In which case you’ll need to charge the standard rate of VAT on the transport.

According to HMRC’s website , this would look like:

- Transport services when they’re included in the admission price to a place of entertainment, historic or cultural interest like a theme park or museum.

- The use of any vehicle to, from or within a place of entertainment, historic or cultural interest, if the transport and admission are supplied by the same or by connected persons

- Transport in any motor vehicle between a car park or its vicinity and an airport passenger terminal or its vicinity, when the car parking facilities are supplied by the same or connected persons

- Flights for entertainment or the experience of flying and not primarily to transport people from one place to another

Usually, passenger transport in a vehicle that can only accommodate less than ten passengers is subject to VAT at the standard rate . The standard rate of VAT in the UK is 20%.

More than ten seats: Probably zero-rated. Less than ten seats: Probably the standard rate. But let's take a closer look.

Is there VAT on Uber and taxis?

Yes, there is usually VAT on taxi fares at the standard rate unless the taxi driver is self-employed and not registered for VAT. So it’s always worth asking for a VAT receipt.

Bear in mind that most Uber drivers are self-employed and earn under the VAT threshold. So you’re less likely to get any sort of VAT return through Uber, whereas lots of taxi drivers work for larger firms that will have to charge VAT.

You’ll also be charged VAT on other parts of a taxi journey like:

- Waiting time

- Administration charges

If you give a tip to a taxi or Uber driver this is not regarded as payment for a supply, so is outside the scope of VAT.

Is there VAT on ferry travel?

So long as the ferry in question can carry more than ten people at a time, they are usually zero-rated for VAT purposes.

There is an exception to this rule for boat rides to, from, or within a place of entertainment or cultural interest. In these cases, the tickets are subject to standard-rate VAT rates. Ferries, canal boat trips, and similar boat excursions that do not have additional facilities and take place on the open sea or other waterways accessible to the public are zero-rated for VAT.

Is there VAT on buses?

VAT rates for buses are just like train tickets and other forms of public transport, zero-rated. Any travel expenses relating to a bus journey must be entered as zero-rated in your accounting software, and not exempt.

But remember in scenarios where the cost of bus fare is included with the right of admission to a place of entertainment or provided by the same provider then it is standard rate VAT.

Is there VAT on coaches?

Coach tickets do not have VAT added to their price because coach travel is considered an essential service that is zero-rated for VAT. However, certain things you buy during a coach journey, like onboard food and entertainment, may have VAT included in their cost.

Is there VAT on flights?

Public flights in the UK are VAT-free, so you don't have to pay or charge VAT on a flight ticket, but they’re not complete tax exemptions. You are subject to Air Passenger Duty (APD) that airlines include in the ticket pricing.

The amount of APD taxation depends on how far you're flying and the class you choose. Domestic flights are taxed for both the outbound and return trips, while international flights are only taxed on the outbound leg from the UK. Unlike VAT, you can't reclaim APD, except when you book a flight but end up not using it. In that case, you can reclaim the APD from the airline by filling out a form.

Private flights with less than ten passengers, or pleasure flights that are designed for an experience rather than transportation, are an exception and still subject to the standard 20% VAT rate.

Ultimately businesses claim all VAT refunds for travel expenses by completing the appropriate sections on their VAT return. If the amount of VAT you’re claiming exceeds the amount of VAT you owe, then the government will pay you back the difference in the form of a VAT refund.

In practice, this looks like:

- Making sure you’re VAT registered .

- Ensuring you have valid VAT invoices for all your postage expenses.

- Keeping accurate records of your input VAT.

- Filing your VAT returns on time and including postage costs.

You’ll then receive a VAT refund that includes VAT charged as part of travel expenses if you’ve shelled out more on VAT for things you’ve had to buy as a business, versus things you’ve sold as a business.

Remember that to be eligible for a refund you must meet all the necessary VAT compliance rules and regulations. HMRC may review your VAT refund claim, and request additional documentation or information to support your claim. So it's essential to maintain accurate records and be prepared to provide any relevant documentation.

If you register for VAT, there are a few different VAT accounting schemes you can use to go about telling the government how much you owe them and they owe you:

- Standard VAT accounting means you track purchases, sales, and VAT amounts, paying or claiming back based on invoice dates every quarter.

- The Flat Rate Scheme simplifies things, using a percentage of your annual turnover to calculate VAT.

- Cash Accounting is similar to standard VAT accounting but everything is based on the payment date, not the invoice date.

- Annual Accounting is for those who prefer filing VAT returns once a year and paying based on invoices.

What’s best for you and your business will depend on:

- Your cash flow

- How much VAT you pay out and get paid

- How large the finance team is in your organisation.

Managing expenses related to travel can be a hassle, especially when it comes to understanding and managing VAT. Pleo can help you:

- Centralise expense data

- Simplify expense reimbursement

- Automate receipts for Tfl journeys

But if you are not ready to go for a software solution just yet, then our expense reimbursement template might come in handy for you.

Smarter spending for your business

Save time on tedious admin and make smarter business decisions for the future. Join Pleo today.

Powered in the UK by B4B partnership

Senior Content Manager

Content, demand gen and SEO professional. 5 years in the CPH start-up scene. Get in touch!

You might enjoy...

.png?ixlib=gatsbyFP&auto=compress%2Cformat&fit=max&dpr=2&w=373 "coach travel zero rated")

The lowdown on professional subscriptions HMRC approves of in 2024

Find out which of your professional subscriptions HMRC approves of and how to get tax relief on them in 2024.

What businesses need to know about HMRC fuel rates for private cars in 2024

Businesses can offset fuel expenses for work-related journeys, but what about if you’re not driving a company car… can the fuel rates still...

What you need to know about HMRC uniform tax in the U.K. for 2024

Discover how you can turn time spent on washing your workwear into billable hours.

Get the Pleo Digest

Monthly insights, inspiration and best practices for forward-thinking teams who want to make smarter spending decisions

You are currently viewing our [Locale] site

For information more relevant to your location, select a region from the drop down and press continue.

Is there VAT on train tickets? (and other common VAT questions)

VAT: what can you claim?

VAT is a tax charged on a range of goods and services that can be purchased for use by a business. If your business is registered for VAT , you can often reclaim this tax as a refund from HMRC by filing a VAT return .

VAT is charged at different rates for different products and services and you can only reclaim what you pay for. Most of the time this means you can reclaim VAT at the standard rate (20% of the cost of the product or service) or at the reduced rate (5%). However, while VAT technically exists on zero-rated products it is charged at 0% - so you don’t pay anything extra and as a result can’t claim anything back!

VAT is one of the most complicated areas of the UK tax system and as a small business owner you might often be left scratching your head over what items are exempt from VAT and what you can claim back. If you’re struggling to figure out what goods and services are exempt from VAT (and therefore what you can and can’t claim VAT back on), this guide will help.

Jump to a section or read on to learn more:

1. Can you claim VAT back on travel?

2. Can you claim VAT back on food and drink?

3. Can you claim VAT back on property?

4. Other common VAT questions

Can you claim VAT back on travel?

Train tickets.

No - train tickets are zero-rated for VAT so you can’t claim anything back.

No - like train tickets and most public transport costs, bus fares are zero-rated for VAT so you can’t reclaim anything on them.

Yes - you can usually claim VAT on taxi fares at the standard rate (20%) unless the taxi driver is self-employed and not registered for VAT - always ask for a VAT receipt. It’s worth noting that the majority of Uber drivers are self-employed and earn under the VAT threshold, so you can’t usually reclaim VAT on Uber fares.

Fuel and mileage

Yes - VAT is charged and can usually be claimed on petrol and diesel at the standard rate of 20% for business travel. If your accounts come under investigation from HMRC , you may be asked to provide a travel log to prove the journey was business related. The log should include:

- where the journey started and ended, including postcodes

- who you visited and why

- the date of the journey

Mileage for business journeys can also be claimed as an expense; you can find out more in our guide to motor expenses . If you’re claiming a mileage allowance rather than the actual costs of your journey, you can only reclaim VAT on the fuel element of the mileage allowance.

Flights/air travel

No - air travel is zero-rated for VAT so you can’t claim anything back.

Car parking

Maybe - street parking is exempt from VAT so you can’t claim back VAT on charges from a parking meter. Private car parks, however, may charge VAT if the car park business is VAT-registered, so you should always check your receipt for a VAT number. If there’s a VAT number on your receipt you should be able to reclaim VAT on parking charges.

Car hire/leasing

Yes - if you hire or lease a car then you can usually reclaim at least 50% of the VAT on the hire fees. You may be able to reclaim 100% of the VAT charge if the car is only used for business purposes and is not available for private use.

Commercial vehicles/company cars

Maybe - you can sometimes reclaim the VAT for buying a car if you use it exclusively for business purposes. HMRC is strict about this, so reclaiming VAT on a car can be a challenge unless in certain circumstances, such as for a taxi or a driving school car. VAT is charged at the standard rate of 20% for almost all new cars and vehicles but this rate may differ for second-hand purchases (see below).

You may also be able to reclaim VAT on a commercial vehicle if it is used exclusively for business purposes. Commercial vehicles include tractors, vans and lorries but you may also be able to reclaim VAT on motorcycles, motorhomes, combi vans and car-derived vans if they are used entirely for business purposes.

Congestion charge

No - as statutory fees, such as the London congestion charge, are outside the scope of UK VAT, you cannot reclaim VAT on them.

Vehicle insurance

No - vehicle insurance is exempt from VAT so you can’t claim anything back.

Second-hand cars

Maybe - cars that are bought and sold privately (i.e. by anyone outside the motor trade), are outside the scope of VAT. However, if a car is bought from a VAT-registered dealership then the tax may apply. The rate of VAT applied may vary due to The Margin Scheme , so it’s important to check your receipt to see how much you’ve been charged.

Maybe - MOTs are outside the scope of VAT, provided that the cost does not exceed the statutory maximum. Any costs over and above the statutory maximum should be expected to be standard-rated for VAT.

Vehicle road tax

No - UK road tax is outside the scope of VAT.

Can you claim VAT back on food and drink?

Maybe - a jar of coffee bought from a shop is zero-rated for VAT, so you can’t claim anything back. However, coffee that is bought as a hot beverage (i.e. from a cafe, restaurant or takeaway) is standard rated at 20%, but you can’t reclaim this VAT if you bought the coffee for the purpose of business entertaining .

No - milk (including soya, rice and coconut milk) is zero-rated for VAT, therefore you can’t claim anything back. This also extends to flavoured milk drinks, including milkshakes.

No - cakes are zero-rated for VAT, therefore you can’t claim anything back. Even if a cake is still warm when it’s sold, it remains zero-rated as it’s not sold with the intention of being eaten hot. If you go ahead and eat it before it cools we promise not to tell!

Bottled water

Yes - bottled water is taxed at the standard rate of 20% for VAT.

Maybe - biscuits are zero-rated for VAT unless they are wholly or partially coated in chocolate, in which case they are charged at the standard rate of 20%.

Yes - chocolate bars, including diabetic chocolate, are standard-rated for VAT at 20%.

Yes - alcoholic beverages (including beer, cider, wine, spirits and liqueurs) are standard-rated for VAT at 20%. Again beware that you can’t reclaim VAT on alcohol bought for the purpose of business entertaining .

Maybe - shop-bought sandwiches, such as those sold in supermarkets, are zero-rated for VAT, so you can’t claim anything back.

Cold sandwiches bought in an eatery such as a cafe or sandwich outlet are zero-rated if they are not consumed on the premises. However, they are charged at the standard rate of 20% if they are consumed on the premises. This is why ‘eat-in’ and ‘takeaway’ prices often differ in cafes.

Hot sandwiches are charged at the standard rate of 20% wherever you choose to eat them.

Restaurant food

Maybe - food purchased and consumed in a restaurant is usually charged at the standard rate of VAT (20%) regardless of whether it’s hot or cold. One exception to this rule is if you buy cold food from a restaurant but don’t eat it on the premises. Again beware that you can’t reclaim VAT on meals bought for the purpose of business entertaining .

Reclaiming VAT on food and drink

In order to claim any VAT on food and drink, HMRC will have to be satisfied that it qualifies as a reasonable business cost - which can be tricky! Our guide to claiming expenses for the cost of food and drink has more information on this topic, but it’s always wise to check with your accountant before claiming any tax.

Can you claim VAT back on property?

Vat on building work and renovations.

Maybe - VAT for most work on houses and flats by builders, plumbers, plasterers, carpenters and similar trades is charged at the standard rate of 20%.

However, building work for a new home or for aiding people with disabilities may be zero-rated for VAT.

Building a new home

Maybe - when building a new home, VAT is likely to be charged on the supply of materials only. However the supply of labour or the joint supply of labour and materials is likely to be zero-rated, so you won’t be able to claim anything back.

You can apply to HMRC for a VAT refund on building materials if you are building a new home or converting an existing non-residential property into a home. This also applies to non-profit communal residences such as hospices. You must apply to HMRC for this refund within three months of completing the work to be eligible.

Estate agent fees

Yes - estate agent fees are charged at the standard rate of 20%. Can you claim VAT on amenities?

Maybe - water supplied to households and most premises is zero-rated for VAT, so you can’t claim anything back. Some businesses in the manufacturing, construction and engineering sectors may be required to pay VAT at the standard rate of 20% for water.

Electricity bills

Yes - VAT is charged at the reduced rate of 5% for the supply of electricity to domestic properties or for non-business use by a charity. Electricity supply for business use is usually charged at the standard rate of 20%.

Yes - VAT is charged at the reduced rate of 5% for the supply of gas to domestic properties or for non-business use by a charity. Gas supply for business use is usually charged at the standard rate of 20%.

Other common VAT questions

Can you claim vat on insurance.

No - insurance is largely exempt from VAT and doesn’t incur any charges beyond Insurance Premium Tax (which is different from VAT), so you can’t claim anything back.

Can you reclaim VAT for bad debts?

Yes - you can reclaim the VAT that you’ve paid HMRC but have not received from a customer if it’s a ‘bad debt’ (i.e. one you do not expect to be paid). To qualify for the relief:

- the debt must be between six and 54 months old

- you must not have sold the debt on

- you must not have charged more than the normal price for the invoice item on which the debt has been incurred

Can you claim VAT on newspapers?

No - newspapers are zero-rated for VAT so you can’t claim anything back.

Can you claim VAT on sales to non-EU countries?

No - VAT is a tax on goods used in the EU. If goods are exported outside the EU they are zero-rated for VAT.

Can you claim VAT on charitable donations?

No - voluntary donations to charity are outside the scope of UK VAT, so you can’t claim anything back.

Can you claim VAT on stationery?

Yes - stationery is usually standard-rated for VAT at 20%.

Can you claim VAT on batteries?

Yes - batteries are usually charged at the standard rate of 20%. Certain batteries can be charged at the reduced rate of 5% when sold alongside a solar photovoltaic system .

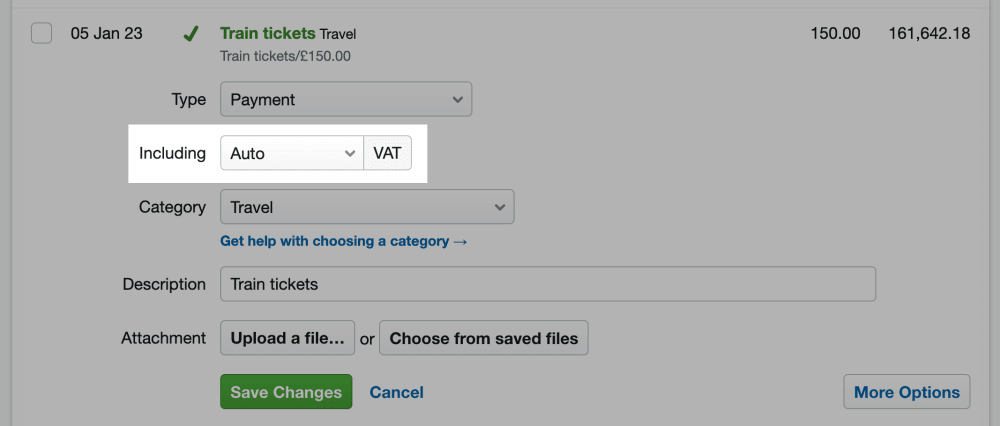

Accounting for VAT in FreeAgent

When explaining bank transactions in FreeAgent, you can select 'Auto' and the software will automatically apply the relevant rate of VAT for the category you're allocating the transaction to. This means that if you know a payment is for travel, you often don't have to worry about knowing the correct rate of VAT off the top of your head. If you do know the correct rate of VAT, you can also select this within the software!

Find out more about online VAT filing with FreeAgent.

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.

Say hello to FreeAgent!

Award-winning accounting software trusted by over 150,000 small businesses and freelancers.

FreeAgent makes it easy to manage your daily bookkeeping, get a complete view of your business finances and relax about tax.

Related articles

- What rate of VAT should you charge?

- The complete guide to charging and reclaiming VAT

Are you an accountant or bookkeeper?

VAT and transport expenses: all you need to know

Magali Sire

Content manager

Updated on 07/08/2023

- Reclaim VAT

The travel costs of running a business can be substantial. This is true for companies of all sizes, from sole traders to multi-national corporations. The VAT regulations governing travel as well as ancillary costs such as accommodation , food and drink, road tolls, parking fees , corporate hospitality, entertaining clients and staff , and offering gifts are complex. It is worth finding out how and what you can reclaim . Find out all about VAT and how it applies to transport with Mooncard.

The provision of passenger transport services

The value-added tax ( VAT ) regulations on the provision of passenger transport services change regularly and it can be difficult for companies to keep up with developments. The latest UK notice on the supply of passenger transport services dates from January 2021. This notice, issued by the UK government, defines passenger transport services as being supplied when “a vehicle, ship or aircraft is provided together with a driver or crew, for the carriage of passengers”.

Passenger transport services include, for example , buses, coaches, trains, canal barges, taxis, ferries and so on, as long as they are provided with a driver. The VAT rate that can be applied to passenger transport services varies. They can either be zero - rated , reduced-rated or standard-rated.

The provision of a service to transport passengers within the UK can be zero-rated with regards to any vehicle, ship or aircraft designed to carry ten or more people, as well as any scheduled flight, and transport provided by the Post Office.

There are exceptions to this rule. These largely relate to the provision of transport to and from a place of entertainment if the same company is providing the transport and the entertainment.

Reduced-rate VAT applies to the provision of transport in the form of cable cars, gondolas and so on, as long as these vehicles are not designed to carry more than nine people.

The provision of taxi services, limousine services and hire cards is covered by the standard VAT rate (20%) unless the vehicle has ten or more seats.

VAT on different forms of transport

The amount of VAT that can be reclaimed on transport depends on the type of transport. Assuming that the purpose of the journey is “wholly and exclusively” connected to the business (visiting a customer , picking up supplies , attending a conference, for example), you may decide to use a number of transport options to complete the journey.

Although many companies now strive to reduce their air miles and use greener forms of transport, flights remain the only feasible option for many business trips, especially when time is of the essence. Domestic flights in the UK are zero-rated for VAT, so there is no VAT that can be claimed back .

The same holds for train tickets , which are also zero-rated for VAT. It is worth remembering that “zero-rated” is not the same as VAT-exempt.

One of the only forms of transport that VAT can be reclaimed on is taxis , but this is only the case if the taxi firm is VAT-registered. As with anything contained in your VAT return, VAT receipts must be provided, so remember to ask for one from the driver!

Finally, you or your employees may decide that it is most convenient to use a personal car to get to the destination, in which case mileage, fuel, and other costs such as parking can be declared as expenses and the VAT is deductible . If you decide to pay a mileage allowance to your staff, you should remember that only the fuel part of the allowance is VAT-deductible, not the part relating to wear and tear on the vehicle.

VAT on freight services

As with the provision of passenger transport services, the VAT regulations applying to the supply of freight transport are complex but worth understanding for companies involved in transporting goods .

The definition of “freight”, according to the UK government, includes the transport of goods or cargo, mail, documents and unaccompanied vehicles. “Freight transport services” are supplied when a vehicle is provided with a driver or crew for the purposes of carrying goods.

In terms of the VAT on freight services, this depends upon where the “place of supply” is. As with passenger transport, when the entire journey takes place within the UK, UK VAT regulations apply. The transport is, therefore, standard rated. Different rules apply when providing transport services between the UK and another country.

Transport outside the UK

If the transport takes place entirely within the UK, obviously the supplies are all considered as being inside the scope of application of the UK’s VAT regulations. However, specific VAT rules are applied to passenger transport that involves journeys that are partly within the UK and partly outside the UK. For example, a boat departing from an English port may transport passengers to Dublin and then return to the UK.

It is essential to determine where the “place of supply” is. In this case, the part of the journey that is within UK territorial waters is covered by UK VAT rules, while the remainder is not. One exception is cruise ships that enter the UK from abroad. These vehicles are considered to be outside the scope of UK VAT, as long as passengers neither embark for the first time nor definitively disembark while in the UK.

The VAT rules around transport, whether involving your staff, passengers or freight, are complex and it is worth finding out more about which rules apply to your situation. A Mooncard corporate card can help streamline your record-keeping and make it easier to file VAT returns and make claims. For more information , get in touch to book a no-strings-attached demonstration from Mooncard today!

Magali Sire is Marketing & Brand Content Manager at Mooncard. An entrepreneur and experienced copywriter, she has been a Swiss Army knife for over 20 years in BtoB and BtoC, research, economic and financial media and retail, and is passionate about the development of support professions.

IMAGES

VIDEO

COMMENTS

You may zero rate your supply when making certain arrangements for a supply of zero-rated passenger transport. You can find further information in Travel agents (VAT Notice 709/6) .

Examples of zero-rated passenger transport. cliff lifts, where the individual cars are designed or adapted to carry at least ten passengers. excursions by coach and train (including steam...

The carriage of a bus, coach or taxi with passengers is regarded as passenger transport, whether or not charged at the private car rate by the operator, and is zero-rated provided the...

Is there VAT on coach travel? Coach travel is listed as a zero-rated essential service, meaning that there should be no VAT charge when travelling via coach.

Coach tickets do not have VAT added to their price because coach travel is considered an essential service that is zero-rated for VAT. However, certain things you buy during a coach journey, like onboard food and entertainment, may have VAT included in their cost.

Can you claim VAT back on travel? Train tickets. No - train tickets are zero-rated for VAT so you can’t claim anything back. Bus fares. No - like train tickets and most public transport costs, bus fares are zero-rated for VAT so you can’t reclaim anything on them. Taxi fares

The rule is that if the method of travel can carry ten passengers or more then it is zero-rated. This means that train, underground and ferry tickets should all be zero-rated.

Zero-rated transport. You can zero rate the transport of passengers: • from a place within to a place outside the UK or the other way around to the extent those services are supplied in the UK – see section 3. • in any vehicle, ship or aircraft designed or adapted to carry not less than 10 passengers to the extent those services are ...

Passenger transport services include, for example, buses, coaches, trains, canal barges, taxis, ferries and so on, as long as they are provided with a driver. The VAT rate that can be applied to passenger transport services varies. They can either be zero - rated, reduced-rated or standard-rated.

The zero-rated domestic passenger transport will also include: • pleasure cruises. • cliff lifts. • excursions by coach or train (including steam railways) • horse drawn buses. • mystery coach or boat trips. • sightseeing tours. • the transport element of park and ride schemes designed to reduce traffic congestion in city centres. Need help?